Aduro Clean Technologies - Updated Investment Thesis

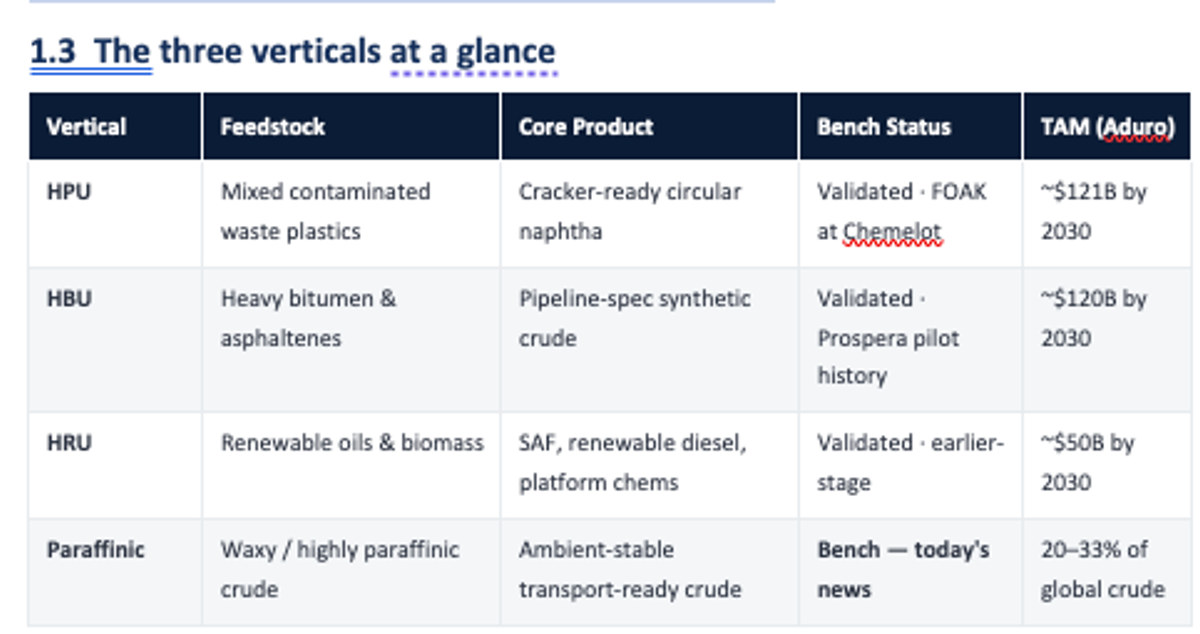

Aduro Clean Technologies has evolved from a niche plastics recycler into a diversified hydrocarbon platform. By extending its water-based Hydrochemolytic Technology (HCT) to paraffinic crude, Aduro now addresses three multi-billion-dollar markets: plastics, heavy bitumen, and waxy oils. With a commercial-scale plant (FOAK) underway at Chemelot and successful bench tests unlocking stranded Uinta Basin reserves, the company is positioned as a policy-aligned leader in energy independence and chemical circularity.

Executive Summary

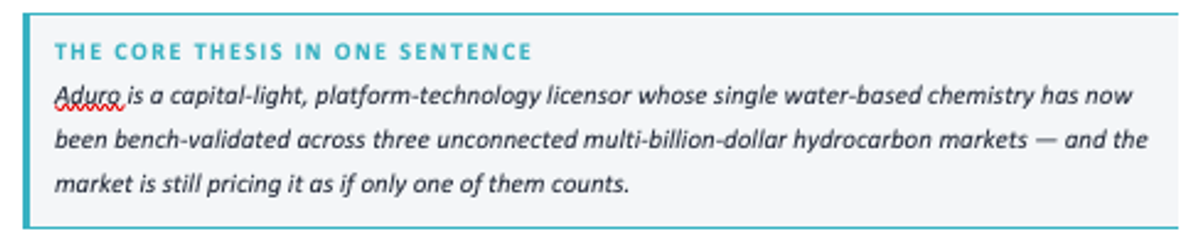

On April 23, 2026, Aduro Clean Technologies filed a continuation-in-part patent application with the USPTO that extends Hydrochemolytic Technology (HCT) to a third distinct class of hydrocarbon feedstock: highly paraffinic (waxy) crude oil. Bench-scale tests on yellow wax and black wax feedstocks from Utah's Uinta Basin reduced wax content and produced a lighter crude that stays stable at ambient conditions.

That phrase stable at ambient conditions is what this thesis update is about. It is also why Aduro is no longer a single-vertical plastics recycling story that happens to have some oil upside. With three distinct hydrocarbon chemistries now responding to one water-based reaction platform, Aduro is a platform technology company with three independent shots on goal, each addressing a market measured in the tens of billions of dollars.

FEEDSTOCKS VALIDATED

Plastics · Bitumen · Paraffinic crude

NEAR-TERM TAM

$250Bn+ Combined addressable, per Aduro

MARKET CAP ~$380M

NASDAQ: ADUR at ~$11.70

The Utah development is specifically the kind of data point that distinguishes a platform from a product. HCT was already validated for waste plastics (Chemelot FOAK, Shell GameChanger graduation, TotalEnergies evaluation, offtake LOI, ISCC PLUS) and for heavy bitumen (Alberta oil sands, Prospera, diluent-penalty economics). As of this morning, HCT is also validated on paraffinic crude, a 20-33 percent slice of global oil production, the fastest-growing stream in North America, and the single most policy-favoured oil play in the United States today. Aduro has just demonstrated, at the bench, a chemistry that attacks the single physical bottleneck holding back Utah's Uinta Basin at the exact moment federal policy and infrastructure investment are converging on that basin.

1. The HCT Platform: One Chemistry, Three Doors

1.1 What HCT actually is

Hydrochemolytic Technology is a water-based, continuous-flow, subcritical-pressure catalytic process. In plain chemistry terms, a liquid metallic catalyst weakens specific C–C bonds in hydrocarbon chains while leaving C–H bonds intact, and a hydrogen-donor co-agent (glycerol, ethanol, cellulose, or other bio-based sources) caps the freed carbons in the same reaction window milliseconds before they would otherwise recombine into tar or char. The process runs at moderate temperatures with water as the reaction medium, eliminating the need for external hydrogen gas.

That last point is worth repeating because the whole economic model rests on it. Every competing upgrading or chemical-recycling technology currently at scale requires either a steady supply of expensive, natural-gas-derived hydrogen or extreme temperatures to drive the same bond cleavage. HCT does neither. It uses water and a sacrificial bio-donor. That is why the process temperatures, reactor sizes, and capital intensities are all lower than those for pyrolysis, hydrothermal liquefaction, or conventional thermal cracking.

1.2 Why a platform, not a product

Most recycling and upgrading companies are single-chemistry, single-feedstock businesses. Pyrolysis operators do pyrolysis on polyolefins. Agilyx does thermal depolymerization on polystyrene. Mura runs supercritical water on mixed plastics at Wilton. Each is a point solution that lives or dies by the economics of a single end market. HCT differs because its underlying reaction mechanism is feedstock-agnostic. The catalyst weakens carbon-carbon bonds, and that mechanism does not care whether those C–C bonds are in a polyethylene polymer, a bitumen asphaltene, or a paraffin wax. Tune the residence time, adjust the temperature, select the right hydrogen donor, and the same reactor architecture addresses three entirely unrelated industries.

The continuation-in-part patent filed today matters not because it adds one more vertical, but because it provides third-party validation in the form of a USPTO application that the platform generalizes. Two bench validations could be a coincidence. Three, on chemistries as different as polymers, asphaltenes, and n-alkanes, are a platform.

For scale: global plastic production runs at 413 million tonnes per year against a 9 percent recycling rate, with less than 1 percent via chemical recycling. The paraffinic crude application sits within the broader HBU framework in Aduro's IP architecture, heavy-oil upgrading chemistry applied to a different heavy-hydrocarbon challenge, but commercially it is a distinct opportunity with distinct counterparties, distinct logistics economics, and a distinct policy tailwind.

2. The Utah Unlock: Energy Independence as the Hook

WHY THIS NEWS MATTERS NATIONALLY

The United States produced 13.6 million barrels of crude oil per day in 2025, an all-time record. Within that record, the fastest-growing single stream, the one attracting the most capital, policy attention, and infrastructure investment, is Uinta Basin paraffinic crude. And paraffinic crude has a single defining problem: it does not flow at ambient temperature.

2.1 The Uinta Basin problem in physical terms

Uinta Basin crude is classified into two grades. Yellow wax has an API of 38-44 and is produced from deeper formations, with a pour point around 120°F. Black wax is 30-34 API, produced from shallower formations, with a pour point around 105°F. Both are exceptionally low in sulphur, metals, and nitrogen, making them highly desirable feedstocks for refiners, but the paraffin content gives them the consistency of shoe polish at room temperature.

The logistics chain that has evolved to move this crude is extraordinary:

• At the lease: the crude is stored in heated tanks held at approximately 170°F.

• First mile: trucked in insulated tanker trailers, roughly 130 truckloads per day per major loading facility to regional rail terminals like Wildcat Loadout and Price River Terminal.

• Long haul: transloaded into insulated coiled railcars that are kept heated in transit to Gulf Coast refineries, crossing multiple mountain ranges.

• Destination: offloaded by pumping steam through the coils of each railcar to re-liquefy the crude so it can flow.

• Refining: processed at only a limited subset of U.S. refineries equipped to handle high-paraffin feedstocks. Salt Lake City has ~205,000 bbl/day of regional demand; beyond that, barrels must reach specific Gulf Coast facilities.

Every barrel from the Uinta goes through some version of that chain today. That chain is not a bug; it is the operating reality of every producer in the basin. And it is the reason production growth in the Uinta is constrained not by how much oil is in the ground (there is a lot), but by how much heated, insulated, coil-equipped logistics capacity exists to get each additional barrel to a refiner that can process it.

2.2 What HCT does to that chain

Aduro's bench tests did one specific thing: they took yellow wax and black wax feedstocks, ran them through HCT, and produced a lighter crude product that stays liquid at ambient conditions. If that result holds at pilot and demonstration scale, the entire logistics chain described above collapses:

• No heated storage tanks at the lease.

• No insulated tanker trucks to the rail terminal.

• No coiled heated railcars on the long haul.

• No steam-coil offloading at the refinery.

• A meaningfully wider set of refineries that can accept the barrel.

This is the same economic logic as HBU in Alberta uses chemistry at the wellhead to eliminate a physical constraint that is currently solved with expensive ongoing operating infrastructure, but the constraint being eliminated is different (wax precipitation vs. viscosity), the counterparties are different (U.S. independent producers and midstream operators vs. Canadian oil sands majors), and the policy environment is an order of magnitude more favourable.

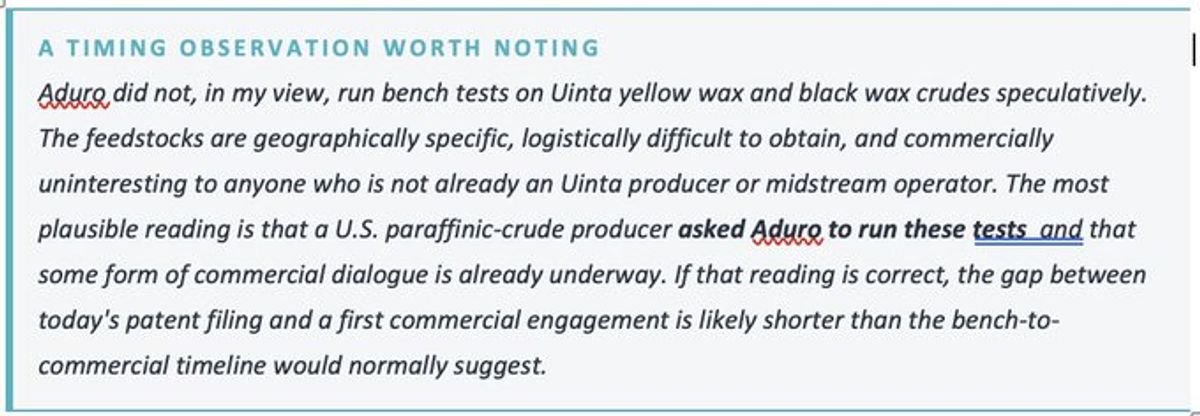

Here is a link that shows what Aduro can do to this waxy material: https://x.com/AduroCleanTech/status/2047353411041976669

2.3 The policy tailwind

The 2025-2026 U.S. energy policy environment is arguably the most producer-friendly in a generation, and the pieces align specifically around Uinta crude:

• The Unleashing American Energy executive order and the National Energy Dominance Council have prioritized domestic crude production as a national-security matter; the Bureau of Land Management subsequently approved the Wildcat Loadout expansion under the national energy emergency designation, clearing additional rail-loading capacity on federal land.

• The U.S. Supreme Court ruled 8-0 on May 29, 2025, in Seven County Infrastructure Coalition v. Eagle County, reinstating the Surface Transportation Board's approval of the 88-mile Uinta Basin Railway a project explicitly designed to connect Uinta production to the national freight network and the Gulf Coast refining complex.

• The Energy Transfer Price River Terminal expansion, announced in October 2025, will add 140,000 bbl/day of loading capacity and accelerate truck offloading for what the industry is now marketing as American Premium Uinta (APU) crude.

Every one of those infrastructure investments exists because paraffinic crude cannot move without heat. Aduro's chemistry, if it scales, does not compete with that infrastructure; it amplifies it. An ambient-stable Uinta product dramatically expands the set of refineries that can take each railcar, removes the steam-coil offload constraint that currently bottlenecks terminal throughput, and extends the commercial reach of every barrel that rolls onto a train.

2.4 Sizing the prize

Put numbers to this. The Uinta Basin contains an estimated 300 billion barrels of oil in place. Of that, only approximately 77 billion barrels are considered technically and economically recoverable today. The balance remains stranded because the cost of transporting the wax-laden barrel to a refinery that can process it exceeds the barrel's value upon arrival. That gap between oil in place and economically recoverable oil is not a geology problem. It is a logistics problem.

If HCT, deployed at commercial scale, made even 15 billion of those stranded barrels pipeline-ready and broadly refinable, that represents approximately $1.2 trillion in gross asset value unlocked in a single basin at an $80 per barrel reference price. Aduro captures a royalty on the per-barrel economic uplift rather than the full asset value, the same model as HBU in Alberta, but the size of the underlying prize determines how many counterparties engage, how quickly commercial dialogue advances, and how aggressively infrastructure flows into the basin alongside the technology.

And the Uinta is the showcase, not the ceiling. Highly paraffinic crudes are 20 to 33 percent of global oil production, with similar pour-point and wax-precipitation problems stranding reserves across Africa (notably Nigeria and Angola), Central Asia, the former Soviet Union, and parts of Southeast Asia. Third-party estimates of the global stranded-paraffinic-crude opportunity reach approximately $4 trillion in potential value creation. The Uinta makes the right commercial showcase because it is tight, visible, and policy-aligned. The global opportunity is what the stock is ultimately priced on if this chemistry reaches commercial deployment.

3. HPU (Plastics): The Near-Term Execution Story

HPU remains the vertical closest to commercial revenue. Every near-term catalyst in the Aduro story, the FOAK industrial plant, the offtake LOI, the EPC MOU, the analyst coverage, and the institutional re-rating thesis runs through the plastics vertical over the next 18-24 months.

3.1 What has happened since the last update

• NGP Pilot Plant commissioned and transitioned to operating campaigns (Q3 FY2026, announced February 2026). The London, Ontario, plant has shifted from project execution to continuous operation, supporting feedstock qualification and performance data generation for commercial scale-up.

• Chemelot Industrial Park selected for the FOAK facility (January 2026). Chemelot provides integrated utilities, shared infrastructure, and proximity to European steam crackers, a textbook FOAK siting decision.

• Ebert HERA B.V. engaged for permitting (April 9, 2026). Ebert HERA is an established Chemelot-ecosystem permitting specialist; the contract signals Aduro is moving into the regulatory application phase rather than merely scoping it.

• Offtake LOI with a leading international commodities trading company (March 12, 2026). The LOI includes a committed offtake arrangement for the initial production parcel from the FOAK plant, the first formal commercial commitment in company history.

• EPC MOU with a leading global engineering and construction organization (March 19, 2026). The MOU covers the joint development of a comprehensive commercial licensing package and a pre-engineered plant concept, which serve as the foundation for a licensing-driven business model.

• ISCC PLUS mass balance certification retained; Aduro joined Chemical Recycling Europe in March 2026, positioning the FOAK plant directly within the policy and certification framework that will govern EU chemical recycling at an industrial scale.

• U.S. public offering completed US$20M + $3M over-allotment, closed December 2025 and January 2026. Cash position CAD $39.42M at February 28, 2026, providing a meaningful runway through FOAK engineering and permitting milestones.

3.2 The competitive moat: nobody else does what HCT does

Global plastic production is approximately 413 million tonnes per year. Only roughly 9 percent is recycled. Mechanical recycling is the dominant pathway today. It handles clean, single-resin, sorted streams like PET bottles and HDPE jugs, and collapses on anything contaminated, coloured, or mixed. That leaves the bulk of the waste stream, mixed polyolefins, multi-layer packaging, and contaminated film, with essentially nowhere to go. Chemical recycling is supposed to address that gap. In practice, chemical recycling accounts for less than 1 percent of global treatment, and the handful of publicly traded competitors are each locked to a single resin or chemistry.

The competitive map is narrower than it looks. The companies most frequently grouped with Aduro in the chemical recycling conversation are not actually doing the same thing:

• PureCycle Technologies (PCT) solvent-based purification for polypropylene only; the commercial Ironton plant is substantially governed by an exclusive supply arrangement with Procter & Gamble, which caps independent capacity growth.

• Agilyx (AGLX) pyrolysis-based, and its Styrenex process requires polystyrene-rich feedstock (>70% PS purity). It is a PS cleanup technology, not a mixed-waste technology.

• Mura Technology the closest architectural analogue, using supercritical water hydrothermal. But Mura requires supercritical conditions (>374°C and >221 bar), which drives minimum-viable plant size north of 100,000 tonnes per year and leaves it exposed to the non-linear scale-up economics that have hurt every thermal-depolymerization peer.

• Carbios enzymatic depolymerization for PET and PET only.

• Loop Industries enzymatic/chemical depolymerization for PET and PLA only.

• Origin Materials focused on PET bottle caps and closures via a proprietary furan-based pathway; a different feedstock category entirely.

• Traditional pyrolysis operators (Quantafuel, Itero, and the various licensed Plastic Energy-style plants) produce unstable olefin/wax mixtures that require downstream hydrotreating to be steam-cracker compatible, and break down on PVC, PET, and food contamination.

HCT is not a better version of any of those. It is a different category. It operates subcritically (lower pressure, lower capital intensity than Mura). It handles mixed, contaminated, multi-resin bales without pre-sorting, because the chemistry routes PVC chlorine into the water phase as salt, routes PET ester linkages through hydrolysis into monomers that separate into the water phase, and routes paper and food residue into hydrogen donors that actually aid the reaction. It produces saturated, cracker-ready hydrocarbons that do not require downstream hydrotreating before entering a steam cracker, a ~$ 400-per-tonne post-processing step that every pyrolysis output undergoes. And it does all of this at yields of 85–95 percent valuable hydrocarbons versus 70–80 percent for pyrolysis.

Said plainly, under the coverage universe, there is no direct competitor. Every other publicly traded chemical recycler is solving a narrower problem with a resin-locked technology. HCT is the only platform positioned to address the ~50 percent of global plastic waste that no existing technology can economically handle, the mixed polyolefin, multi-layer, contaminated stream that mechanical recycling rejects and pyrolysis cannot cleanly handle.

3.3 Why the plastics story is more than plastics

Even setting aside the competitive moat, the strategic reason to care about HPU in the near term is that it is the commercial proving ground for the entire platform. A FOAK plant that operates at Chemelot on mixed contaminated waste plastics and produces ISCC PLUS certified circular naphtha for European steam crackers does two things simultaneously: it generates the first recurring royalty revenue in company history, and it validates the licensing model that will be deployed across HBU, HRU, and the paraffinic crude application.

The EU regulatory tailwind is not a speculative policy bet. PPWR is a binding regulatory requirement that creates structural demand for certified circular naphtha independent of commodity oil prices. That demand is what makes the FOAK economically attractive even in a soft WTI environment, and it is why the offtake LOI counterparty was willing to commit to the initial production parcel before the plant is even built.

4. HBU (Heavy Oil): From Alberta to Utah

4.1 The Alberta base case

The HBU thesis in Canada is unchanged. Canadian oil sands bitumen requires roughly 30 percent diluent by volume to meet pipeline specifications, the diluent penalty with total economic drag widely estimated at $13-21 USD per barrel. HBU attacks that cost structure by chemically upgrading the bitumen at the wellhead: breaking asphaltene chains rather than diluting them, producing a crude that meets pipeline specs (API > 19) with minimal or no diluent, while removing >90% of nickel and vanadium and >30% of sulphur. At a $1.75-$2.25 per barrel royalty on ~3 million bpd of Canadian oil sands production, even a single-digit-percent market share generates tens of millions in annual high-margin licensing revenue.

4.2 The Utah extension reframes HBU as a North American story

Until today, HBU was principally an Alberta thesis with secondary reach into Venezuelan heavy, Mexican Maya, and specific Middle Eastern grades. The continuation-in-part filing changes that. HBU is now a North American heavy-hydrocarbon upgrading platform with two distinct commercial showcases: Alberta (viscosity problem, diluent cost structure, Canadian majors as counterparties) and Utah (wax-precipitation problem, heated logistics cost structure, U.S. independents and midstream as counterparties, Uinta Basin Railway and Gulf Coast access as policy tailwinds). Different customers, different economies, different physical problems, same underlying chemistry. The engineering team that designs an HBU upgrader for Alberta bitumen does not start from scratch when the next project is a wax-reduction unit for a Vernal, Utah producer. Reactor architecture, hydrogen-donor supply chain, process control, and licensing framework all carry over.

5. HRU (Renewables): The Under-Priced Optionality

HRU remains the least-discussed of the three verticals and, in this writer's opinion, the most under-priced relative to its eventual contribution. The application uses HCT chemistry to deoxygenate bio-oils, such as cooking oil, tallow, and canola, as well as cellulose-derived intermediates, into hydrocarbon-range products suitable for Sustainable Aviation Fuel (SAF), renewable diesel, and platform chemicals. The competitive advantage mirrors the other verticals: conventional renewable fuel pathways require large volumes of external hydrogen to strip oxygen from bio-feedstocks, which is expensive and energy-intensive. HCT's use of water and in-situ hydrogen equivalents from bio-donors eliminates the external-H₂ supply chain, just as it does for plastics and heavy oil.

Demand is structural rather than cyclical. ReFuel EU Aviation mandates rising SAF blend rates across European airports, and U.S. LCFS credits create premium pricing for renewable diesel and SAF that meet carbon-intensity thresholds. HRU is earlier-stage than HPU or HBU; the author's base-case assumption is that it remains in advanced research for the next 24-36 months while the company concentrates execution capital on the FOAK plastics plant. It is in the model at zero and should be treated as pure optionality.

6. Valuation Framing and Near-Term Catalysts

6.1 What is in the price and what is not

At approximately $11.70 per share and a ~$380M market capitalization on roughly 33-35M fully diluted shares, ADUR is priced as a plausibly successful pre-revenue plastics chemical recycler. The implied valuation reflects:

• A reasonable probability of FOAK commissioning on the 2027 timeline. Partial credit for the offtake LOI, the EPC MOU, and the broader commercialization narrative.

• A discount for execution risk, financing risk on FOAK construction capex, and the fact that the company has yet to generate recurring revenue.

• Zero credit for HBU and now the Unita vertical

• Essentially zero credit for HRU and zero credit for the paraffinic crude application announced today.

6.2 Why the paraffinic validation matters to valuation, even pre-revenue

The author's view is that the paraffinic crude bench data does not materially move the near-term cash flow model. It should materially move the platform multiple that a sophisticated investor applies to the stock.

Pre-revenue, thesis-driven stocks trade on a combination of (a) probability-weighted terminal value of the base case, and (b) the option value the market assigns to adjacent expansion. A single-vertical plastics recycler is valued almost entirely on (a). A three-vertical platform technology company with demonstrated cross-feedstock validation earns a meaningful (b). The Utah data does not change (a); it substantially strengthens the argument for (b).

6.4 Risks and honest caveats

This is a pre-revenue micro-cap with real execution risk. The specific risks worth naming:

• Financial position is solid for the current stage. Cash position of CAD $39.4M at February 28, 2026, funds NGP pilot operations, FOAK engineering and permitting, and commercialization activities through the critical 12-month window. The specific financing structure for FOAK construction capex project finance, strategic partner co-investment, or some combination will be defined as FID approaches, and is a milestone to watch rather than an unresolved risk.

• Scale-up is the single largest technical risk gate. Continuous-flow pilot data must replicate batch results, and paraffinic crude remains a bench result. The NGP pilot is designed precisely to surface these risks; the development timeline for a genuinely new vertical is measured in years, not quarters.

• Analyst coverage includes both independent and paid IR. D. Boral Capital ($46 PT, Buy), H.C. Wainwright ($22 PT, Buy), and Ladenburg Thalmann ($19 PT) are independent sell-side. Water Tower Research is a paid IR engagement beginning April 1, 2026 and should be read as visibility support, not independent research.

• Competition exists. Mura Technology's supercritical-water hydrothermal recycling is operational at Wilton at ~20 kta. HCT's subcritical continuous-flow architecture is technologically differentiated, but it is not the only chemistry targeting these markets.

7. The Bottom Line

For two years, the bull case on Aduro was built on one vertical and two hopes: plastics-recycling chemistry that worked, and oil-upgrading chemistry that might eventually scale. As of April 23, 2026, continuation-in-part filing, the bull case is built on a platform with three distinct bench validations across three entirely different hydrocarbon chemistries, and the third of those validations happens to land squarely on the single most policy-favoured, infrastructure-constrained oil stream in the United States.

The plastics story continues to execute on the timeline management has laid out. The Chemelot FOAK remains the single most important 18-24 month milestone, and its successful commissioning will re-rate the entire business. Nothing about today's news changes that.

What today's news changes is the shape of the opportunity behind the FOAK. A successful FOAK is no longer the end of the story; it is the opening chapter of a three-vertical licensing business whose addressable market is measured in hundreds of billions of dollars, whose chemistry has now been validated against three unrelated feedstock classes, and whose third vertical aligns with an explicit U.S. national energy-independence priority.

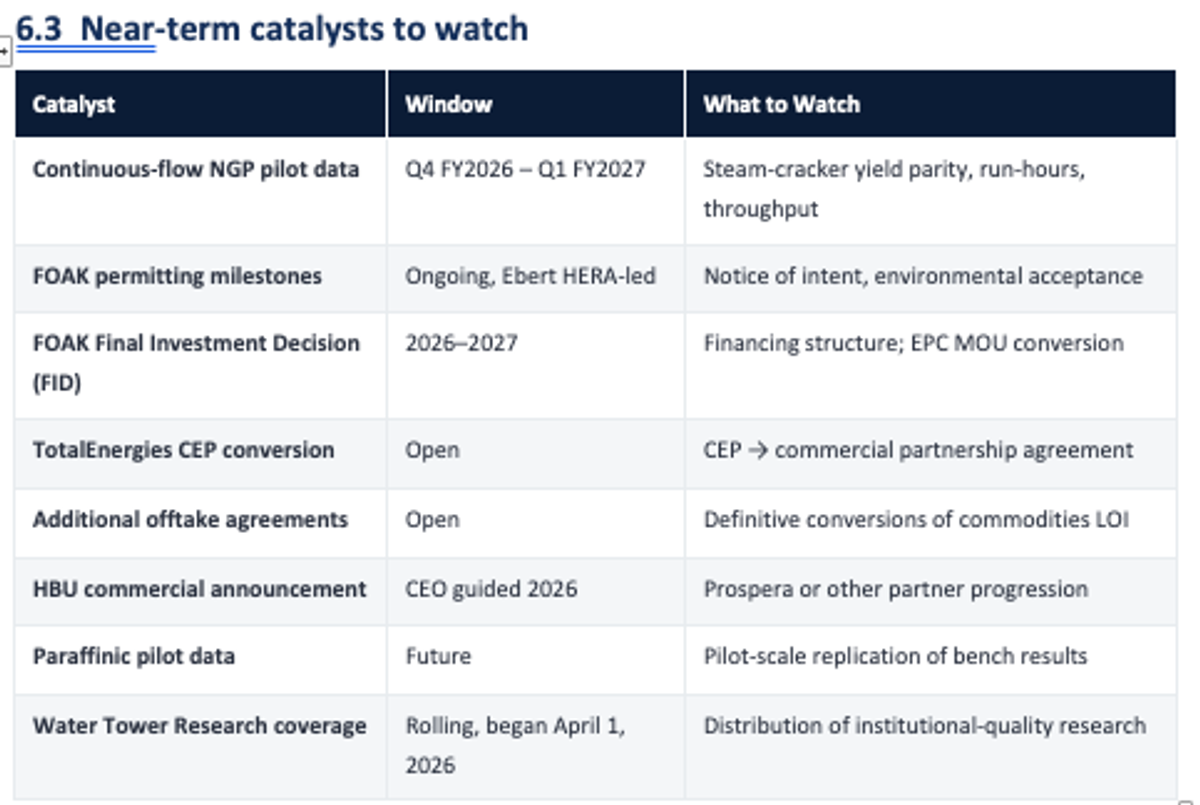

The market is not yet pricing this as a platform. At some point, the author's view is that the inflection arrives with the continuous-flow NGP data release and the conversion of at least one CEP into a definitive commercial agreement, it will.

DISCLOSURES

The author has held $ADUR since the IPO round, and maintains a significant position. This document is for informational and educational purposes only. It is not investment advice, a recommendation to buy or sell any security, or a solicitation of any kind. The author is not a registered investment advisor. All figures are sourced from Aduro public disclosures, SEC and SEDAR+ filings, EIA data, Utah Geological Survey publications, U.S. Supreme Court documents, and third-party news releases referenced in the author's research notes. Do your own work.

This article reflects personal research and opinions and is provided for informational purposes only. It is not financial advice, a recommendation to buy or sell any security, or a consideration of your individual circumstances. Investing in small-cap and pre-commercialization companies involves significant risk, including the risk of total loss. Always do your own research and consider speaking with a qualified financial professional before making investment decisions.

Stay Informed with The Wire

Get the latest insights and analysis on public companies delivered directly to your inbox.