Why This Is My Most Bullish Article on Aduro Yet

Investor Penny Queen argues Aduro Clean Technologies’ hydrochemolytic process could outperform conventional plastic recycling and expand into upgrading paraffinic crude oil. The article highlights aligned management incentives, modular licensing economics, and massive potential markets, while acknowledging the technology remains early-stage, with key partnerships, pilots, and commercial economics still unproven today.

Disclosure first. Read it before you read anything else, so you can filter what comes after.

Before you read another word, here is my bias

Aduro Clean Technologies is my largest personal investment. Ever. Bigger than anything I have held before, by a wide margin.

I met Ofer Vicus, the CEO, before the company went public. Sat across from him for a long, in-depth Q&A on the technology back when it was nowhere near where it is today. I knew a lot less about plastic recycling and hydrocarbon chemistry then than I do now. What I walked away from that meeting with was not conviction in chemistry. It was faith in one man’s determination and principles.

I learned the officers of Aduro had structured their own equity to success. They voluntarily gave up their shares and would only earn them back, milestone by milestone, as the company de-risked. Year after year, they have hit those milestones, unlocked value for investors, and have earned back that equity. And not one of them has sold a single share. Plus they keep buying.

That tells you something about what they think this is.

For context… I trade stocks. I look for disruptive technologies. Last year, my average peak gain across my published picks was 232%. The year before, it cleared the low 300% range. I do not buy fancy cars. I do not build fancy homes. I find more winners. And I keep buying more Aduro.

This is going to be my most bullish article on Aduro to date. I am telling you that upfront so you can filter every claim that follows.

I am not telling you what to do. Investing is always risky. But this is my highest-conviction stock, and I believe that in 10 years, Aduro shareholders will be sitting on a position that has gone up by many multiples. I have said this over and over. I am saying it again.

Now let me show you why.

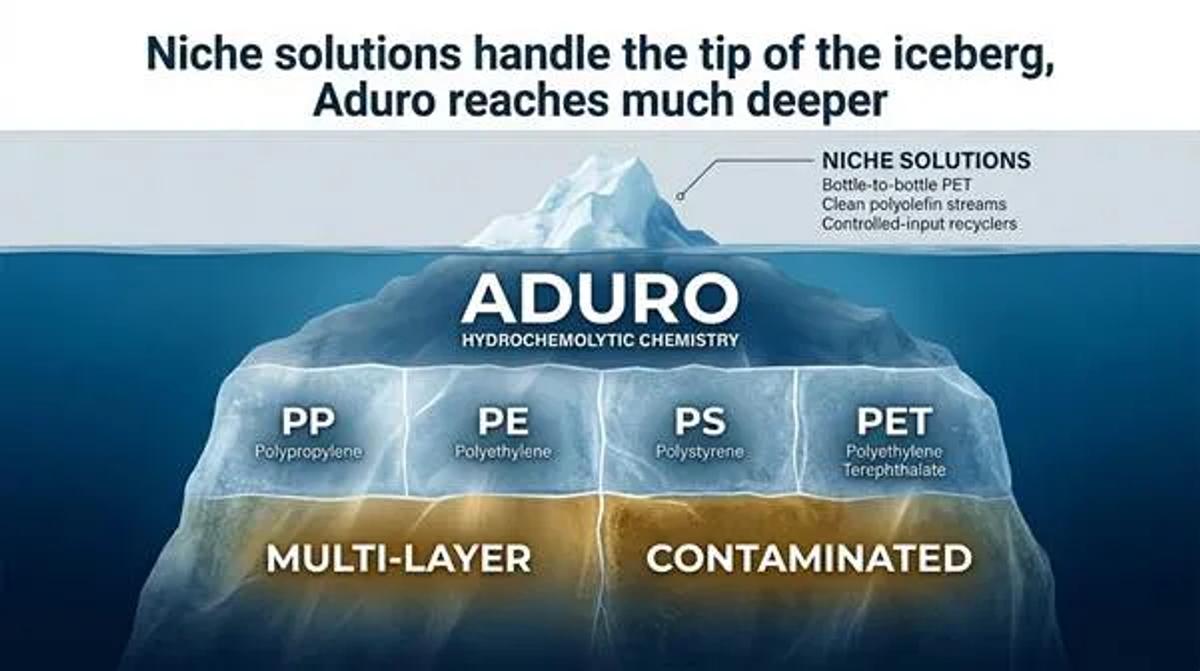

Plastics is the iceberg

When it comes to plastic recycling, we are going to need several technologies. Not one winner. Several.

Plastic is a growing problem, and the chemistry of waste plastic is wildly varied. Clean monomer streams. Contaminated streams. Multilayer films. Mixed polymer bales. Residue-laden flexibles. No single technology handles all of that economically. Anyone who tells you otherwise is selling something.

Here is how I think about the recycling landscape.

The niche solutions are the tip of the iceberg. They handle one specific plastic very well. Bottle-to-bottle PET. Certain polyolefin streams. Controlled-input pellet recyclers. They work. They scale within their niche. Past that niche, they don’t.

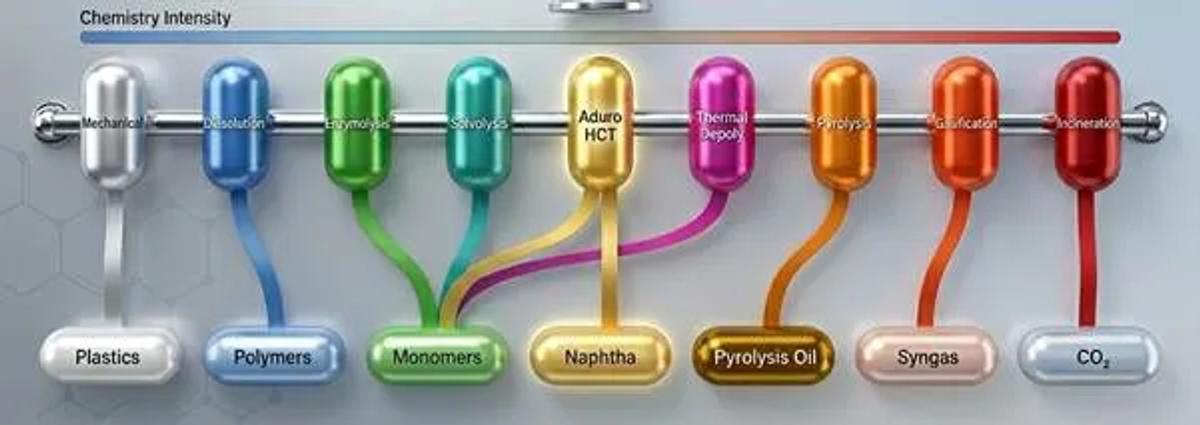

Pyrolysis sits in the middle. It handles a lot of plastic. But the chemistry is essentially blindfolded. Heat breaks the long chain at random spots. The output is a chaotic soup. Some chains end up at five carbons. Some are at fifty. Some carbons get capped with hydrogen. Some are left dangling and reactive. The product needs expensive hydrotreatment before any steam cracker will accept it. It works, but the output is crude, and the economics suffer for it.

Aduro’s technology goes well below the waterline. Hydrochemolytic chemistry does not hack at the chains randomly. It selectively breaks the carbon-to-carbon bond and donates a hydrogen atom in the same step, capping the broken end immediately. The result is stable. The result is a high-quality oil, naphtha-grade for polyolefins like PE and PP, (plus styrene monomer recovery from PS). All of it cracker-ready. No hydrotreatment required Meaning at least a saving of $400 to $600 per ton recycled in operating expenses and a significant Capex reduction as Hydrotreatment requires a massive Capex to be built.

What matters to me as an investor is that Aduro can handle what the rest cannot. Multilayer plastics. Contaminated plastics. The messy, real-world streams that niche solutions reject and that pyrolysis can take but process into low-value outputs. Aduro’s chemistry was designed for the actual plastic waste problem, not the cherry-picked clean stream.

And the business model is just as important to me as the chemistry.

Aduro’s commercial model is modular and scalable. The same plant architecture can be sized to meet a customer’s needs and deployed across different geographies. The company plans mainly to expand through licensing partnerships, not by continually raising capital and building everything itself. Which means future growth does not come from the backs of existing shareholders. That single structural choice materially changes the dilution math over the next decade.

That alone would be a thesis I could believe in.

But that is just plastics.

Thanks for reading Penny Queen’s Newsletter! Subscribe for free to receive new posts and support my work.

Subscribe

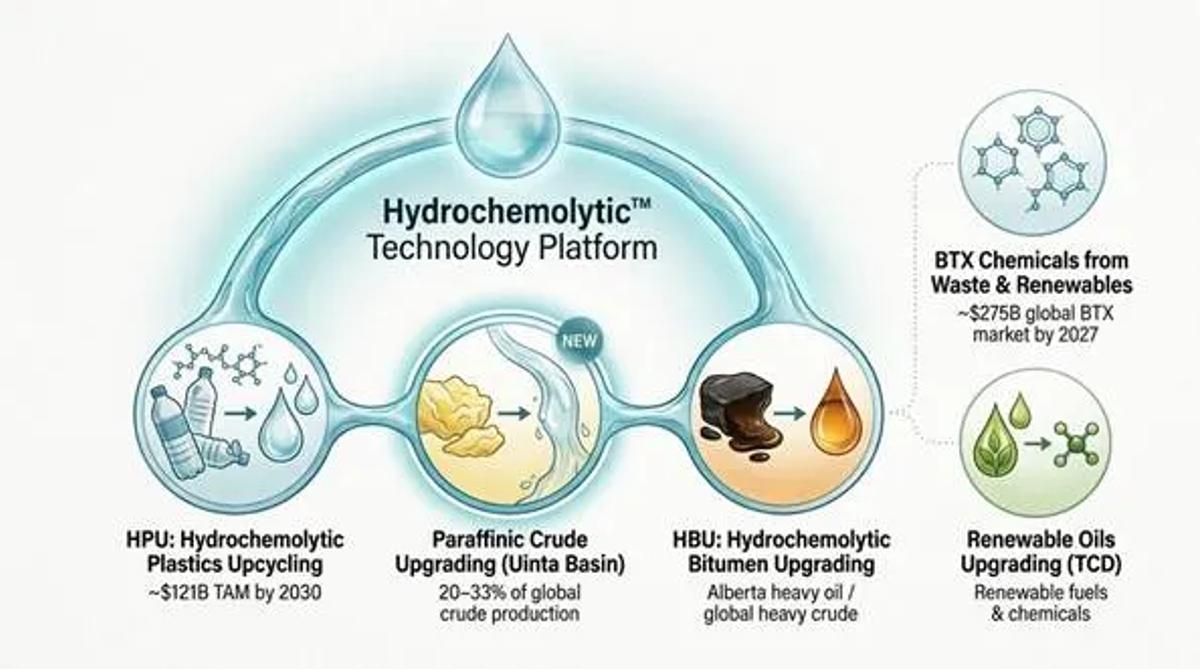

The platform

Aduro’s chemistry is not a plastics-only chemistry. It is a molecular toolkit that applies to multiple long-chain hydrocarbon problems across multiple industries.

The same reaction pathway has now been validated on:

- Plastic — long polymer chains, broken to naphtha-grade output. The HPU vertical, roughly $121B TAM by 2030.

- Bitumen — Heavy oils (like in Alberta, Venezuela, Russia and Kazakhstan) long aromatic and asphaltenic structures, upgraded for handling and transport. The HBU vertical.

- Paraffinic crude — long, straight-chain hydrocarbons. NEW. Bench-scale validated April 23rd, 2026. Continuation-in-part patent filed with the USPTO.

- Renewable oils — the TCD vertical, on the roadmap.

Plus an extension into BTX chemicals from waste and renewables, a roughly $275B global market by 2027.

The newest vertical is what I want to spend the rest of this article on. Because if it pans out, it could be larger in absolute scale than plastics.

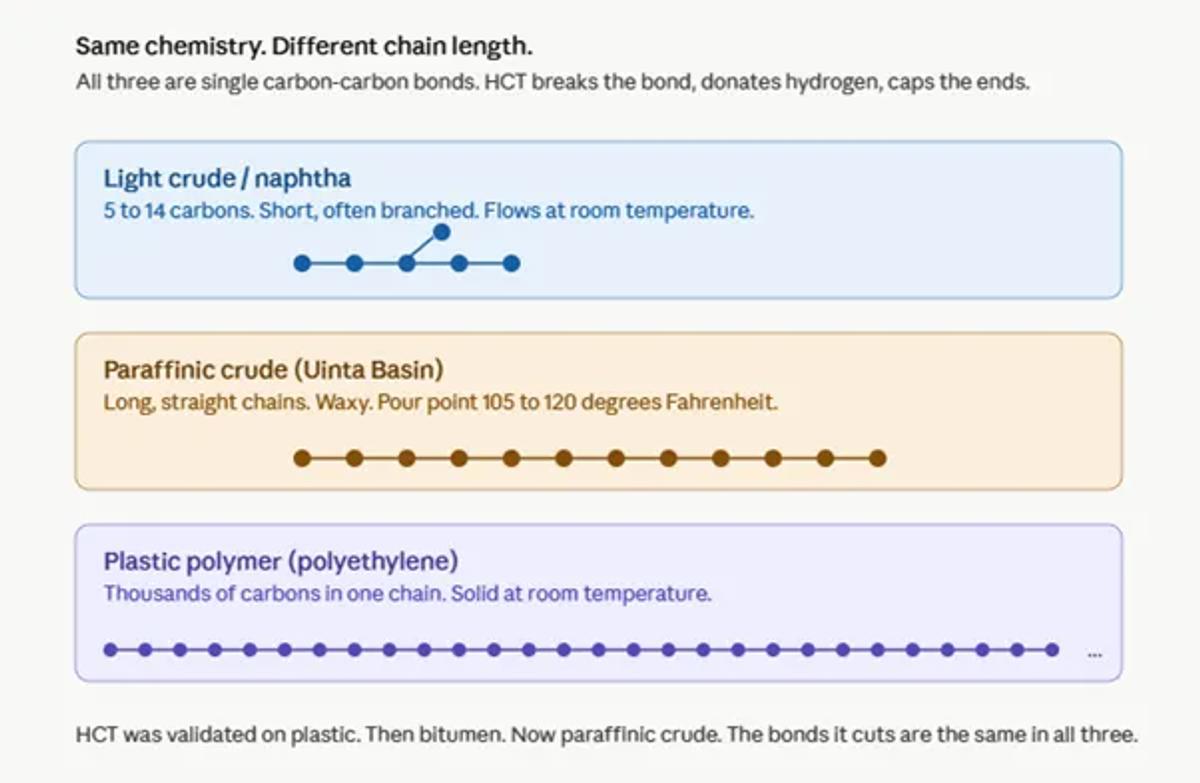

A short detour into chemistry

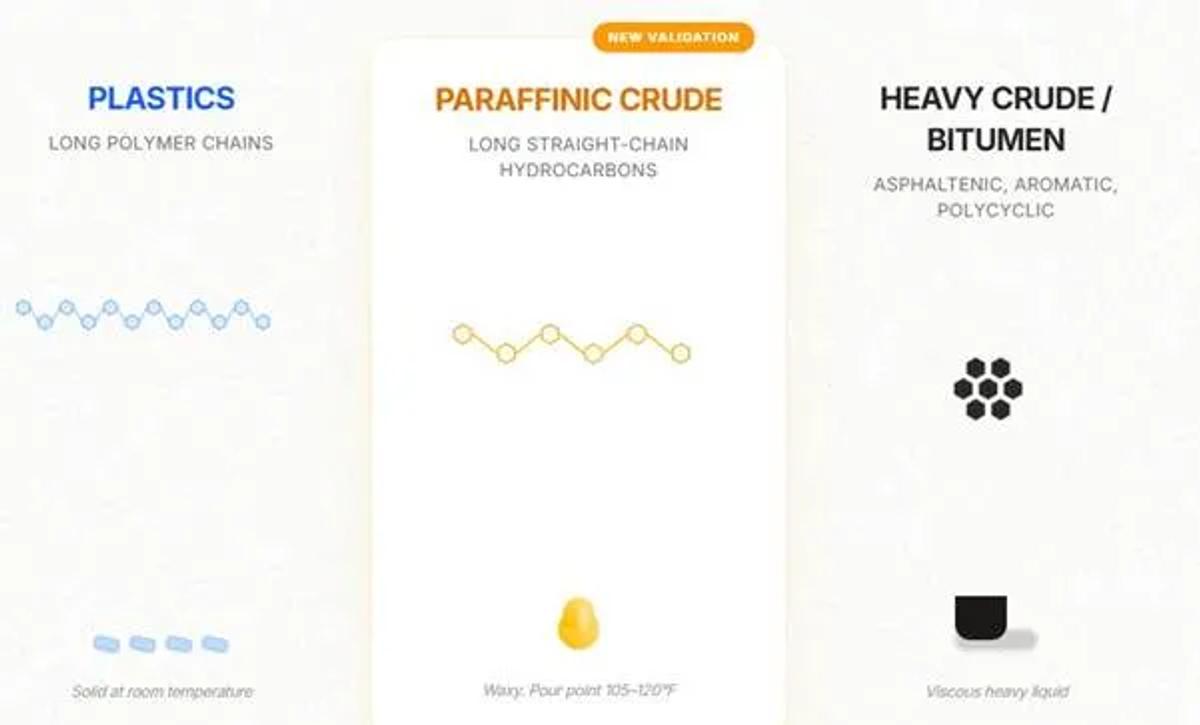

If you have watched the interview I did with the team at Aduro’s London, Ontario facility, you already know the basics. Plastic is a long chain of carbons holding hands. Thousands of carbons. All single-bonded. Stable, but stuck.

Paraffinic crude is the same molecular shape. Just shorter.

Long, straight chains of single-bonded carbons. Twenty or thirty per chain. Long enough that the stuff behaves more like wax than like oil. Pour point around 105 to 120 degrees Fahrenheit. The Uinta Basin in Utah is the textbook example, producing roughly 185,000 barrels a day in 2025.

From a chemical point of view, paraffinic crude is a simpler version of the same problem that HCT was built to solve. The bonds are already single. The chain is already straight. HCT cuts fewer of them, donates hydrogen at the cut points, and lets the result flow.

Same trick. Shorter chain. Same stable, flowable output.

What this could unlock globally

This is the part I want every reader to sit with.

Twenty to thirty-three percent of the world’s oil supply is paraffinic. That is between 16 and 27 million barrels a day.

Almost no one is fully accessing that supply on equal economic footing with light crude. They can’t. Every barrel of paraffinic crude has to be moved with heat. Insulated railcars. Heated storage tanks. Steam-coiled offloading equipment. Specialized refineries are close enough to take the feedstock without choking on it. The crude itself does not change price at the wellhead, but every dollar spent getting it from there to a buyer adds up to a structural penalty that lighter crude simply does not pay.

That penalty does three things. They all matter.

It shrinks the buyer pool. If the only refineries that can handle your wax are within heated-rail or trucking distance, your basis differential to global pricing widens. Operators take a discount on what would otherwise be excellent oil. Uinta Basin is the textbook case. High-quality crude by chemistry. Market access constrained by physics.

It strands marginal acreage. Wells that would underwrite at light-crude transport costs fail to underwrite at paraffinic transport costs. The resource is there. The economics are not. Some of it never gets developed. Some of it just sits in the ground waiting for a better answer.

It limits the global market. Paraffin-rich streams across Africa, Asia, and the former Soviet Union face the same physics. Same transport tax. Same buyer-pool problem. Same suppressed development. This is not a Utah problem. It is a global problem hiding inside a global resource.

So, when I say 20 to 33 percent of the world’s oil supply is “locked up”... I mean it.

Not shut in geologically. Structurally penalized in a way that suppresses development, narrows markets, and discounts the product. A vast global oil pool exists, has buyers in principle, and currently does not compete on equal economic footing with conventional light crude.

If HCT can upgrade paraffinic crude at or near the wellhead so it flows through unheated infrastructure, the impact is not transporting costs.

It is access.

You unlock buyers. You tighten the basis. You make the stranded acreage economic. You let producers who were structurally penalized compete on chemistry rather than logistics. And you do it with a chemistry platform that has already been validated, in adjacent form, on plastic and on bitumen.

That is the prize Aduro is now formally pointing at. And it is enormous.

What has not happened yet

I am not going to walk away from honest framing just because I am bullish.

What got validated on April 23rd was bench-scale. Yellow wax and black wax samples from the Uinta Basin. Reduced wax content. Stable at ambient conditions. Real lab result. Real patent filing. Last week, they also made a key hire Scott Smith to advance petroleum application.

What has not happened yet: no pilot timeline announced. No Uinta Basin partner named. No commercial agreement disclosed. No published economics on cost per barrel processed or on pricing into upgraded-barrel destination markets.

That is normal at this stage. The patent gets filed first. The partner conversations come second. Pilot announcements come after that.

What I am watching from here. Any named Uinta Basin operator partnership. Pilot or demonstration unit announcements specific to paraffinic feedstock. Disclosed unit economics. Capex framing on whether paraffinic upgrading deploys via the same FOAK template as plastics, or via a smaller, modular, wellhead-adjacent unit.

The next twelve months will tell us a lot.

Why I keep buying

Let me close where I started.

Same lab. Same chemistry. Three validated feedstocks, two at industrial development stage and one fresh from the bench. One filed patent extension. One global market opportunity that has been structurally locked up by physics for as long as there has been an oil industry. One management team that voluntarily put their equity behind milestone vesting, hit the milestones, and has not sold a share. One licensable, modular business model that does not grow at heavy shareholder expense.

This is the kind of moment that quietly reframes a company. From “interesting plastics chemistry” to “molecular toolkit operating across multiple industries with global TAM and an aligned management team.” From a single TAM to a stack of independent ones, each with its own customer base and its own urgency.

I have been an Aduro shareholder for a long time, well before this announcement. After it, I am not selling. I am buying.

Pay attention.

Thanks for reading Penny Queen’s Newsletter! Subscribe for free to receive new posts and support my work.

Subscribe

Disclosure

I hold a personal position in Aduro Clean Technologies (Nasdaq: ADUR / CSE: ACT / FSE: 9D5). It is my largest individual investment. I have conducted multiple CEO interviews with the company in the past as part of my editorial coverage. This article is for informational and educational purposes only and is not financial advice. I am not an investment advisor. Investing in the stock market carries substantial risk, including the potential for total loss of capital. Past performance on any of my published picks is not indicative of future results on any individual stock, including this one. Always do your own due diligence.

This article reflects personal research and opinions and is provided for informational purposes only. It is not financial advice, a recommendation to buy or sell any security, or a consideration of your individual circumstances. Investing in small-cap and pre-commercialization companies involves significant risk, including the risk of total loss. Always do your own research and consider speaking with a qualified financial professional before making investment decisions.

Stay Informed with The Wire

Get the latest insights and analysis on public companies delivered directly to your inbox.