The Pick and Axe of Sports Betting

GOAT Industries offers venture-style exposure to sports betting infrastructure through its subsidiary BetSource, a patented “Shazam for sports” technology powering real-time betting, ads, and data. Targeting tribal casinos first, BetSource monetizes via SaaS, revenue share, and data. It’s a higher-risk, early-stage picks-and-axes play in a $150B market.

During the 2025 gold rush in AI, I heard the same phrase over and over: “Don’t buy the gold miners. Buy the picks and axes.” The idea is simple, when everyone is rushing toward an opportunity, the real money is in selling the tools.

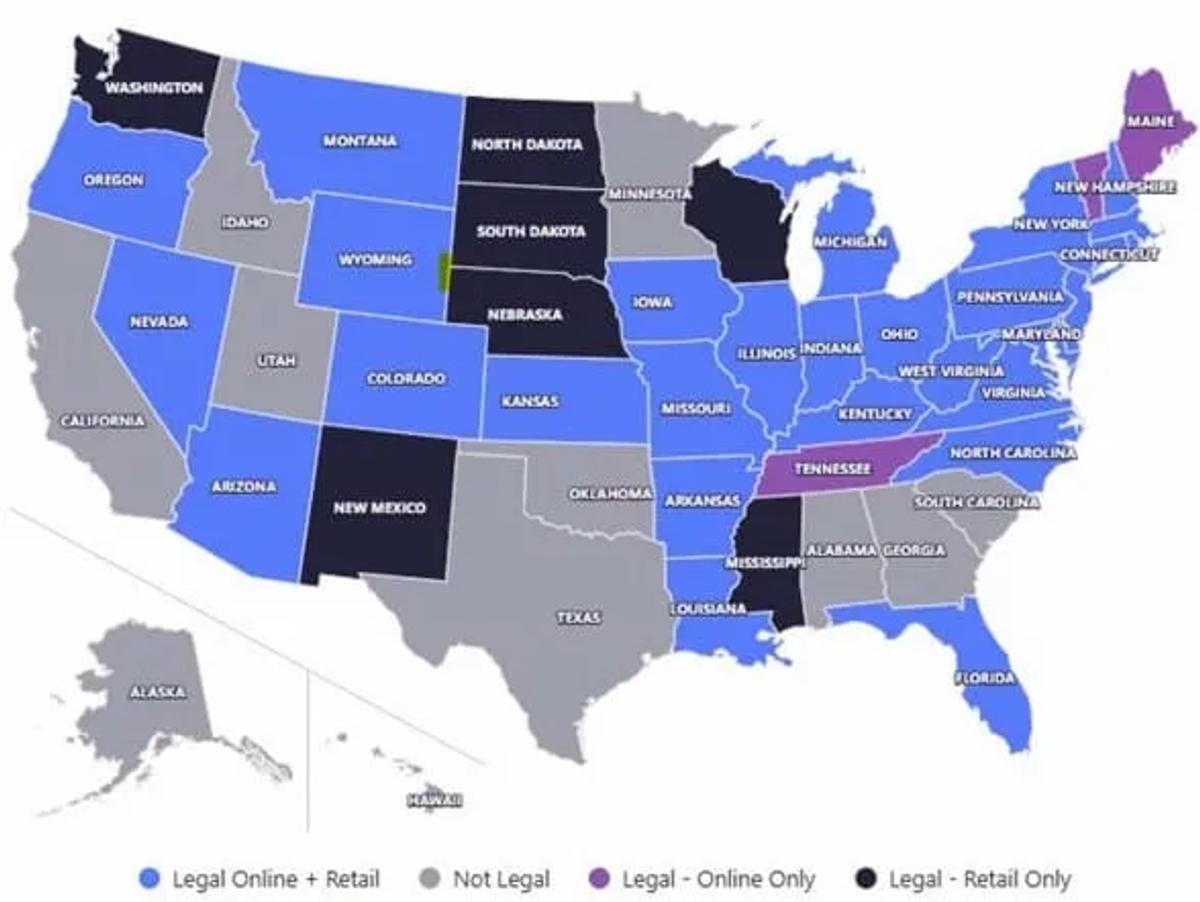

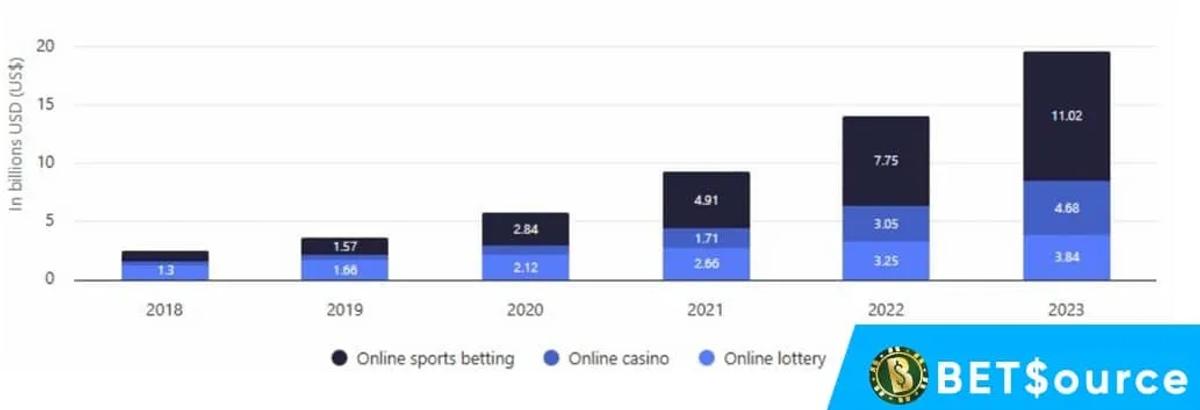

Sports betting in the United States is a $150 billion market and still growing. Online betting is now legal in 38 states. The sportsbooks, DraftKings, FanDuel, BetMGM, are the miners. They’re the ones fighting over customers, burning cash on advertising, competing on odds, and grinding each other down on margins.

So where are the picks and axes?

That’s what interested me in GOAT Industries (OTCQB: BGTTF/CSE: GOAT ) and its wholly-owned subsidiary, BetSource.

What GOAT Actually Is

Before we get into BetSource, I need to explain something about GOAT that confuses people at first: it’s not a typical operating company. GOAT is structured as an investment issuer on the Canadian Securities Exchange, essentially a publicly traded holding company that acquires and develops high-potential businesses.

This is the part that actually got me excited before I even understood the technology. Investment issuers are, in my view, the closest thing retail investors can get to venture capital. You’re buying into a vehicle that sources deals, acquires early-stage companies, and builds them out , the same thing VC firms do behind closed doors for accredited investors. Except here, you can buy shares on the open market.

GOAT owns 100% of BetSource. When you buy shares of GOAT, you get direct exposure to BetSource’s technology, revenue, patents, and growth. And as GOAT continues building its asset portfolio, both organically and through acquisitions, that exposure compounds.

I now have two companies with this investment issuer structure in my portfolio. I think retail investors are sleeping on this model.

The Technology: Like Shazam for Sports Betting

Here’s what BetSource actually does, in plain English.

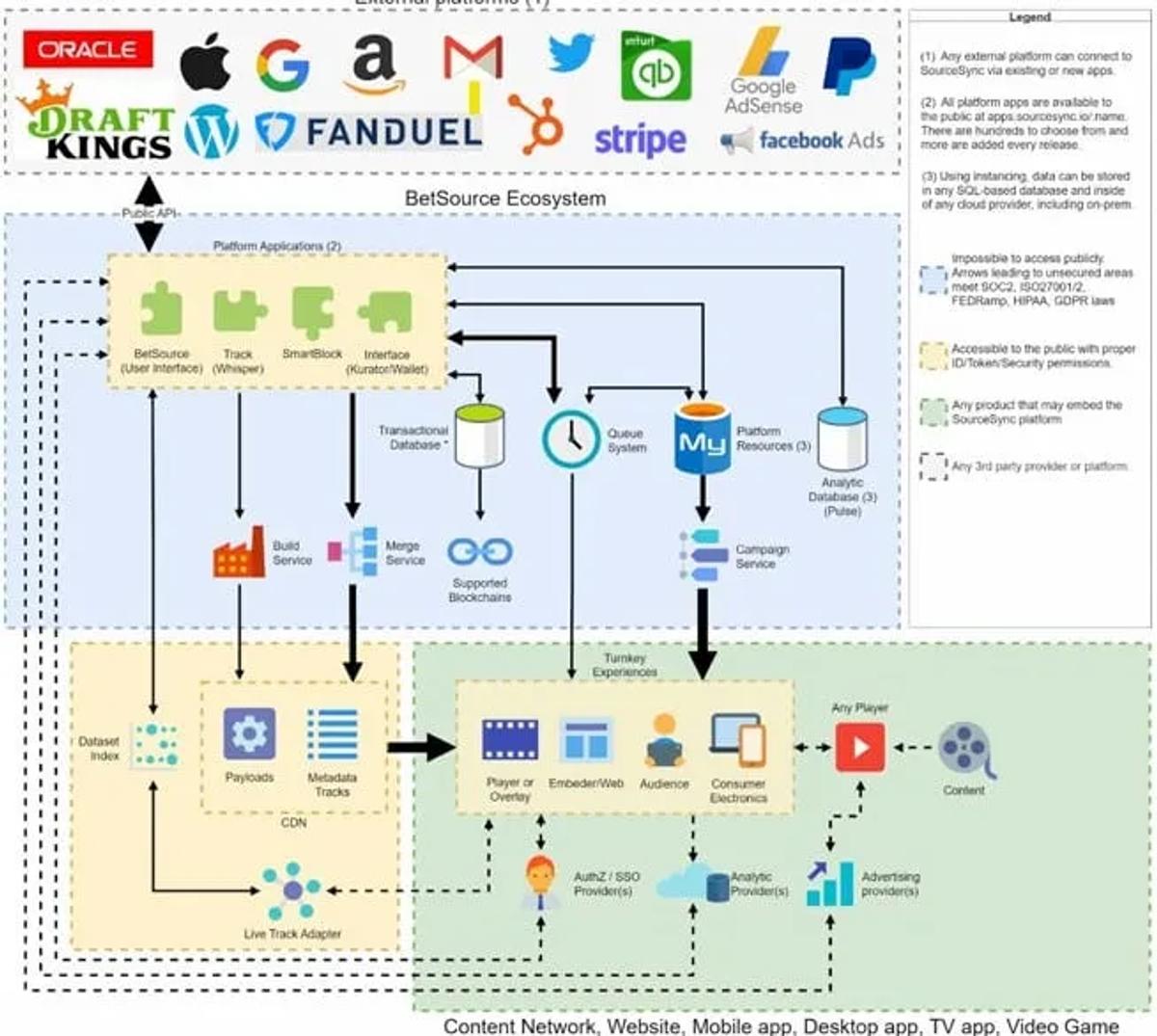

You’re sitting on your couch watching a game. Your phone is in your hand. BetSource’s technology - built on 11 utility patents - listens to the live broadcast audio and identifies exactly what game you’re watching, what’s happening in real time, and what moment you’re in. Think about how Shazam identifies a song playing in a bar. BetSource does the same thing, but for live sports, and instead of telling you the song title, it opens the relevant betting markets, delivers real-time stats, and serves contextual information, all synchronized to the exact moment in the broadcast.

This works across TV, mobile, desktop, and in-venue environments. It’s not a single-screen experience. Whether you’re watching on your living room television and using your phone as a second screen, or you’re sitting in a casino sportsbook with screens on every wall, BetSource adapts to the environment.

And here’s what matters most from an investment perspective: BetSource is not a sportsbook. They are not competing with DraftKings or FanDuel for your bet. They’re the technology layer underneath… the infrastructure that sportsbooks, casinos, and content platforms can plug into to make their own products better. When Hank Frecon, BetSource’s Acting President, described it on Stock Therapy, he put it clearly: “They’re not competitors. They’re clients we want to obtain one day.”

That distinction is everything. BetSource doesn’t need to win the sportsbook wars. They just need the sportsbooks to keep fighting, and to sell tools to both sides.

How They Actually Make Money

This is the part that isn’t in the video, so let me walk through it.

BetSource has three revenue streams that come online in sequence, each one bigger than the last.

Stage 1 (Now): SaaS Licensing.** Casinos and sportsbook operators pay to license BetSource’s technology platform. This is recurring revenue, predictable, scalable, and the foundation of the business. Their stated target is $7.5 to $10 million in annual recurring revenue by the end of 2026. When I asked Hank directly where the pipeline stands, he said they have “a pretty healthy pipeline,” have already had “some great wins,” and that they’re “not shy or afraid of that number.”

Stage 2 : Revenue Share. This is where the model gets really interesting. Instead of flat licensing fees, BetSource begins taking a percentage of the actual betting handle processed through its platform. When you’re sitting in the tech layer of a $150 billion industry and taking a slice of every transaction you facilitate, the math changes dramatically. A SaaS licensing business might be worth $50 to $70 million. A toll booth on betting handle is a fundamentally different valuation conversation.

Stage 3 : Data Monetization. (.This is a more of a blue-sky revenue stream, but very possible with heavy adoption.) As more operators deploy BetSource’s platform, the system starts collecting behavioral data, what users watch, when they bet, what types of wagers they prefer. This data, anonymized and aggregated, becomes a Consumer Data Platform that has significant value to advertisers, content owners, and the operators themselves. This is the flywheel: more users generate more data, which makes the platform more valuable, which attracts more operators.

For the business as a whole, I described it to Hank as being “first a SaaS licensing company, and then beyond that, a toll booth on the $150 billion betting industry.” He pushed back slightly on the toll booth analogy, then paused and said, “I actually like your toll booth analogy.” It’s more like infrastructure that reduces friction, good for every player in the ecosystem, not extractive from any one party.

The Ad Density Concept

One thing that really stuck with me from my research: traditional television gets roughly 30 to 37 ad breaks per sporting event. That’s it. Google serves approximately 240 ads per hour. Facebook serves 62 per hour.

BetSource’s approach is to bring internet-level ad density to the live sports experience - but without interrupting the game. Within seconds of a big play, BetSource can simultaneously trigger a betting opportunity, serve a contextual ad, and surface relevant content, all as part of the viewing experience rather than a break from it. The monetization density is dramatically higher than traditional broadcast, but the viewer doesn’t feel like they’re being advertised to because the information is additive.

As Hank put it: TV has great content, but terrible utility. The internet figured out that you need to monetize both. That’s fundamentally what BetSource is solving for sports.

BKFC: The Proof Point

BetSource holds interactive rights for Bare Knuckle Fighting Championship. If you’re not familiar with BKFC, here are the numbers: 35 million social media followers, a streaming deal with DAZN, 80+ international events per year, and Conor McGregor as an investor. The sport is legal in a growing number of states and has lower injury rates than UFC or football.

This is a fast-growing content property, and it’s a live proof of concept. BetSource technology went live at KnuckleMania VI, BKFC’s biggest event, at the sold-out Xfinity Center in Philadelphia.

Why Tribal Casinos Are the Beachhead

BetSource’s initial go-to-market focus is tribal casinos, and this is a strategically smart entry point that I think investors are underappreciating. Tribal gaming generates more wagering volume than Las Vegas, but these operators were largely left behind when sports betting went digital. The major apps are locked up by DraftKings and FanDuel. The tribal casino market is underserved by modern technology, and hungry for it.

BetSource has partnered with AAMBE Media, a respected aggregator and solutions provider in the tribal casino space, giving them a distribution channel into a market with less competition, real demand, and operators who are motivated to adopt new technology.

It’s a classic beachhead strategy: prove it works in an underserved market, build the case studies and revenue base, then expand to larger operators. Less competition, real need, and a partner who already has the relationships.

What I’m Watching For

Over the next 12 months, I’m looking for operator announcements to tell me whether this thesis is working or not. Every new casino or sportsbook contract validates the pipeline and gets them closer to the ARR target.

I’m also watching for when financial details start coming out publicly. BetSource confirmed they have revenue, with more detailed information expected around the end of Q1 or beginning of Q2. That will be the first opportunity for the market to start valuing this company based on actual numbers rather than projections.

The Bottom Line

I think GOAT Industries represents a rare setup for retail investors: a publicly traded vehicle that gives you venture-capital-style access to an infrastructure play in a $150 billion market. BetSource isn’t trying to win the sportsbook wars, they’re selling the tools to everyone who is. Patented technology, multiple revenue streams that scale from SaaS to revenue share, content rights, and an underserved market as the entry point.

This is early-stage, the company is pre-profitability, and execution risk is real. But I put my own money in at $0.30CAD because I believe in the thesis, and I’ve been buying more in the open market because nothing I’ve learned since has changed my mind.

Do your own homework. Watch the full interview on Stock Therapy. And if you have questions, you know where to find me.

— Penny

Disclosures

I am long GOAT Industries (CSE: GOAT / OTCQB: BGTTF). I participated in the private placement at CAD $0.30 per share with warrants exercisable at CAD $0.45, and I have purchased additional shares in the open market. I want the stock to go up. You should factor that into everything written above.

45 Degrees Inc., a related company, has been contracted by 1502655 B.C. LTD to provide advertising services for GOAT Industries commencing on 02/02/2026 at $30,000 USD per month for a period of 6 months. This is my own research, my own thesis, published on my own Substack. I am not being compensated to write this.

I and/or related parties may buy or sell securities of GOAT Industries at any time without notice. These relationships create material conflicts of interest. You should assume such conflicts exist and conduct your own due diligence.

Nothing in this article constitutes investment advice. All investments carry risk, including the potential loss of principal. Past performance does not guarantee future results. Always do your own due diligence.

This article reflects personal research and opinions and is provided for informational purposes only. It is not financial advice, a recommendation to buy or sell any security, or a consideration of your individual circumstances. Investing in small-cap and pre-commercialization companies involves significant risk, including the risk of total loss. Always do your own research and consider speaking with a qualified financial professional before making investment decisions.

Stay Informed with The Wire

Get the latest insights and analysis on public companies delivered directly to your inbox.