Goat Industries $BGTTF: The Thesis Just Changed In the Best Way

GOAT Industries’ BetSource thesis has strengthened after securing its first commercial monetization deal with a U.S. horse racing and OTB network via Aambé Media. The platform is evolving from sportsbook technology into an in-venue advertising network capturing revenue and data for venues. The partnership opens tribal gaming distribution opportunities, reducing key execution risk. While still speculative, scalable deal replication could materially improve revenue potential and investor returns.

DISCLOSURE: Long $BGTTF. This document is for informational purposes only and does not constitute financial advice. All investments involve risk, including the possible loss of principal. The author holds a position in the securities discussed.

The Thesis Just Changed: In the Best Way

When I first published my investment thesis on GOAT Industries / BetSource ($BGTTF), the core argument was straightforward: the technology was real, the market problem was real, and at a sub-$20M market cap, the stock was pricing in near-total failure. The pivotal event we identified as the critical de-risking milestone was the first commercial contract.

That milestone has now arrived.

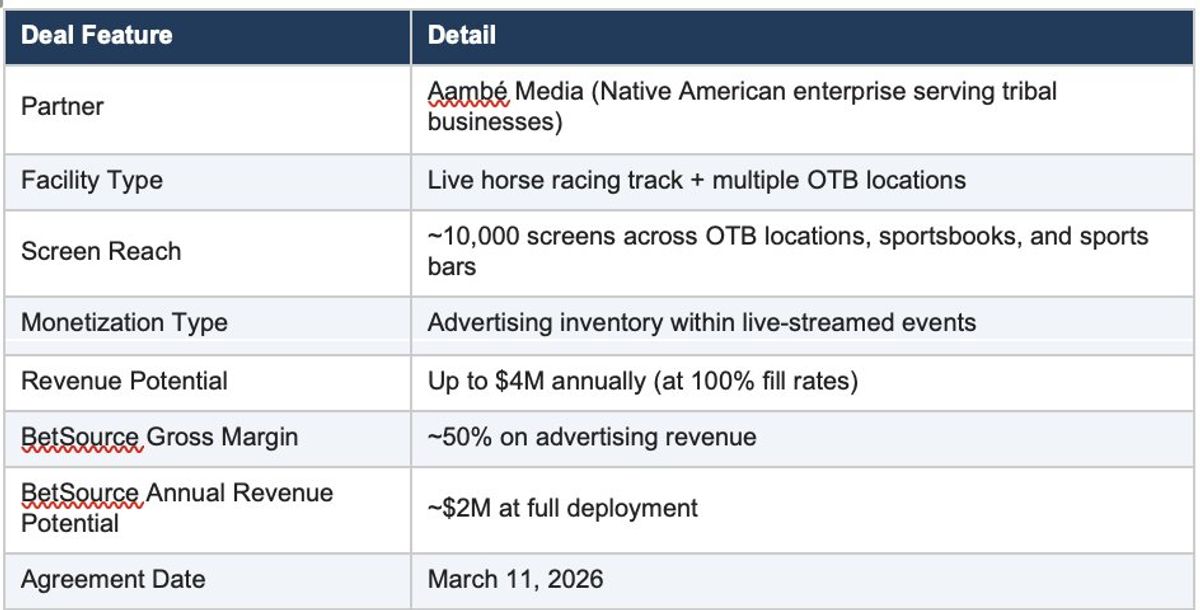

On March 16, 2026, GOAT announced that BetSource had entered into a monetization agreement with a US sports entertainment facility, a live horse racing track with Off-Track Betting (OTB) locations, in collaboration with Aambé Media, a Native American enterprise. The deal targets up to $4 million in annual advertising inventory across approximately 10,000 screens, with BetSource realizing approximately 50% gross margins on such amounts.

The thesis has not changed. The risk profile just improved materially.

A New Way to Understand What BetSource Actually Does

Our original thesis framed BetSource primarily as a casino technology play, an in-house sportsbook and content aggregator designed to recapture betting revenue being lost to mobile giants like DraftKings and FanDuel. That framing is accurate, but it undersells the business model.

In a conversation this week, CEO Kevin Cornish offered a more intuitive analogy that crystallizes the monetization logic immediately:

"BetSource is like Facebook for these venues, casinos, BKFC, horse tracks, and more to come. These venues want to buy from BetSource/GOAT ads to get additional revenue at the door. Think of how Facebook ads get sold to advertise a business. The same goes for BetSource. It advertises the venue and event, and for that, they make money every time."

This is the key mental model shift. BetSource is not only a sportsbook technology company but also an advertising network operator that operates within high-engagement, wagering-friendly environments. The venues are not just deployers of the technology; they are advertisers within the BetSource ecosystem, paying to reach the audiences sitting inside their own buildings.

Think about what Facebook built: a platform where businesses pay to reach audiences at scale, with Facebook capturing a margin on every dollar spent. BetSource is building the same loop, but the "feed" is live sports broadcast across 10,000+ screens in OTB locations, sportsbooks, and sports bars, and the "advertisers" are the venues themselves, local businesses, and event promoters who want to reach that highly engaged, high-intent audience.

The Problem the Market Still Does Not Fully Appreciate

The scale of revenue extraction currently happening at the expense of venues is striking. Cornish put it directly:

"The upside to the venue is that most of these bets currently can't be monetized, or are monetized by third parties that take a maximum 8% of the revenue, in the case of casinos, and keep the rest, as well as the consumer data. So the venue is basically screwed despite the client coming through their door."

Let that sink in. A patron walks into a casino, sits down, watches a live game on the casino's screens, screens the casino paid for, cable subscriptions the casino pays monthly, and places a bet through a DraftKings or FanDuel app. The casino receives nothing. The mobile operator captures 100% of the economics and retains the consumer data.

In the rare cases where a casino does participate in a revenue-sharing arrangement with a third-party wagering operator, it might receive 8% of gross gaming revenue from bets placed on its floor. The operator keeps 92%, plus all the consumer data, which is arguably the more valuable long-term asset.BetSource flips this equation. By deploying the platform inside a venue, the venue becomes the operator. They capture the advertising revenue directly. They retain the audience data. They sell local inventory to businesses that want to reach their patrons. And as their in-house sportsbook capability matures, they can recapture the wagering revenue, too.

Breaking Down the Aambé Media Deal

The first commercial monetization agreement is with a US-based live horse racing facility with multiple OTB locations, announced March 16, 2026, via newswire. The structure is worth examining carefully:

Important caveat: The $4M figure assumes 100% ad fill rates, which is an optimistic ceiling rather than a guaranteed floor. Actual results will depend on advertising demand, fill rates, and market conditions. The company has been explicit about this in its disclosure.Even at heavily discounted rates, assume 40% fill rates in year one. This deal alone would generate approximately $800k in BetSource revenue at 50% gross margins, or roughly 400k in gross profit from a single relationship. At a sub-$20M market cap, investors are paying very little for each incremental deal of this nature.

The Aambé / Tribal Gaming Angle Is Strategically Important

The choice of Aambé Media as the intermediary partner is not incidental; it is a deliberate strategic foothold into one of the most structurally underserved segments of the gaming market.

Aambé Media is a Native American enterprise that serves businesses through partnerships with Native American tribes. Tribal gaming operations in the United States number over 500 properties and represent a uniquely compelling BetSource target:

• Many tribal casinos operate under gaming compacts that limit their participation in statewide mobile sportsbook markets, meaning the third-party extraction problem is acute and hard to solve otherwise.

• Tribal operations often have strong community ties and local patron bases, exactly the audience profile where localized advertising and in-house sportsbooks create the most value.

• A trusted intermediary like Aambé Media dramatically reduces the sales cycle friction for BetSource in approaching these properties.

• OTB facilities like the racetrack in this deal are the natural first deployment environment: screens are already installed, audiences are already wagering-engaged, and the content (live racing) is already streaming.The Aambé relationship creates a distribution pathway into a 500+ property segment through a single trusted intermediary. If BetSource replicates this deal across even a fraction of Aambé's tribal network, the revenue implications are significant.

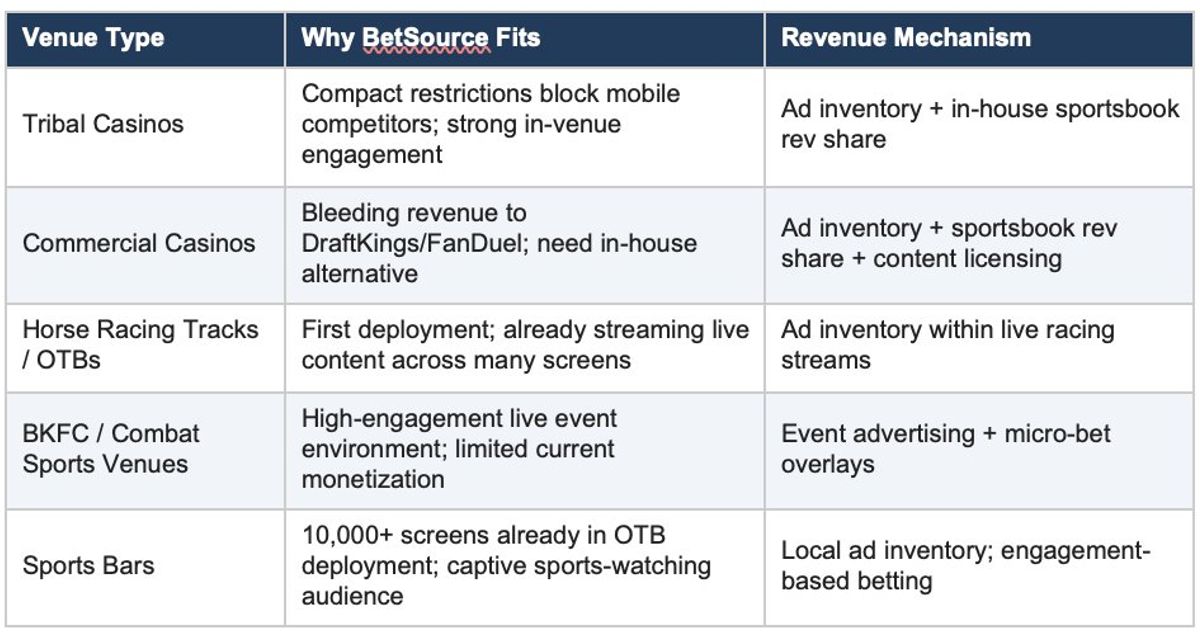

The Market Is Bigger Than Casinos

My original thesis focused on the casino segment as the primary addressable market. The Aambé deal and the CEO's framing this week clarify that the addressable universe is substantially wider:

The Facebook analogy is most useful here: Facebook did not just serve one type of advertiser. It built infrastructure that any business could use to reach its audience. BetSource is doing the same for live sports environments, and the number of potential venues across casino floors, OTB networks, sports bars, and emerging combat sports venues runs into the tens of thousands in North America alone.

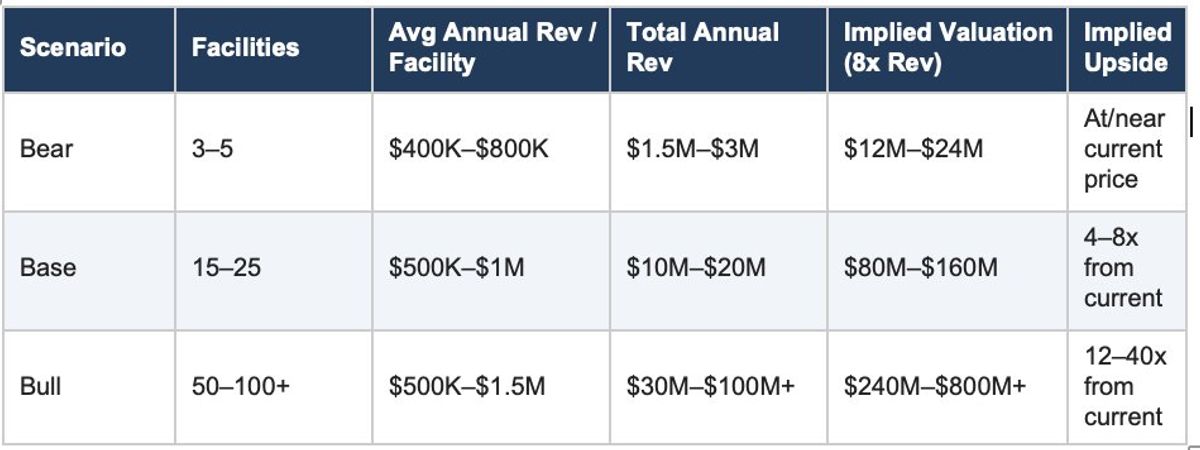

Updated Scenario Analysis

Our original scenario analysis modelled licensing revenue from casino contracts only. With the Aambé deal in hand and a clearer picture of the advertising revenue model, we can update the framework. Note these remain back-of-envelope estimates, not formal guidance.

Methodology note: Revenue per facility reflects a blend of advertising inventory revenue (primary), sportsbook revenue share (secondary), and content licensing. The valuation multiple (8x) is applied conservatively, given the early-stage and OTC listing. As the business matures and delists to a senior exchange, a higher multiple would be more appropriate.

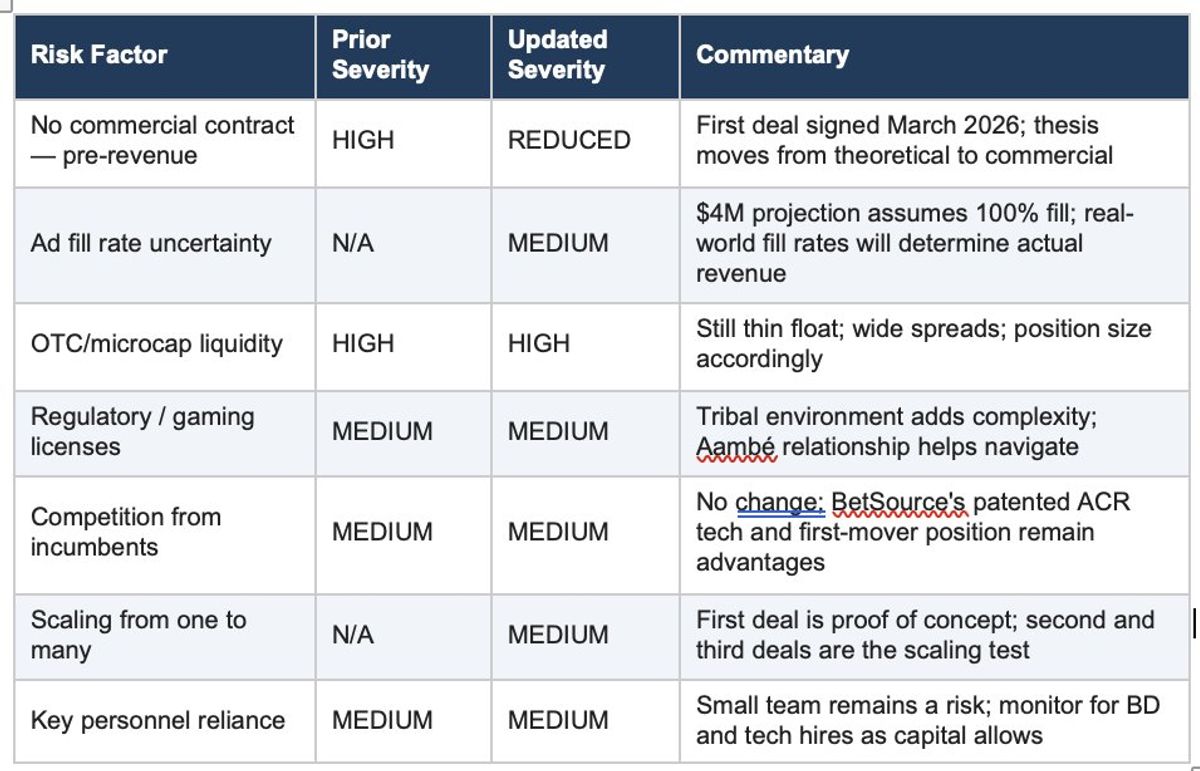

Risk Update

The original risk table identified execution risk, the absence of any commercial contract, as the highest-severity concern. That risk has now been partially mitigated. Here is the updated picture:

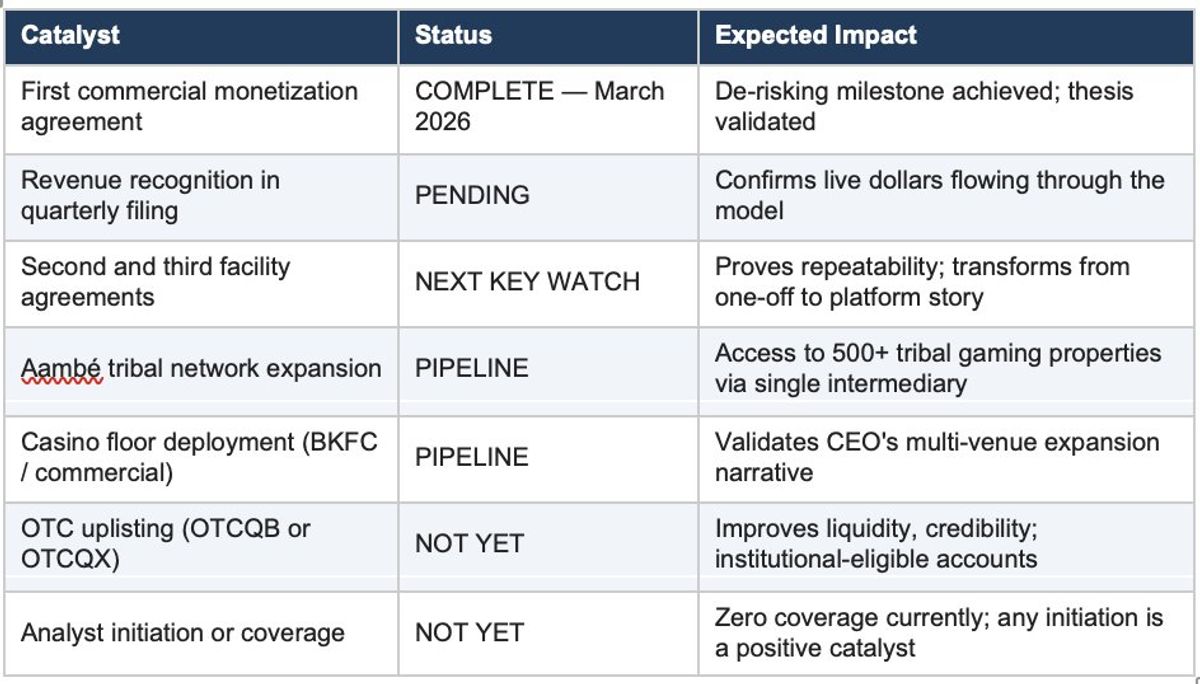

Updated Catalyst Calendar

The catalyst map has shifted. The first deal is signed, and the attention now shifts to how quickly BetSource can scale across additional facilities and prove out the revenue model in practice.

Conclusion & Updated Investment View

The GOAT Industries/BetSource thesis has advanced to the next stage. The most critical de-risking event, a first commercial contract with real revenue economics, has now occurred. The Aambé Media partnership gives BetSource a beachhead in the tribal gaming segment, a distribution pathway into hundreds of additional facilities, and live proof of concept for the advertising monetization model.

The CEO's Facebook analogy is the key conceptual unlock for understanding where this is going. BetSource is building an advertising network inside high-engagement live sports venues, venues that have historically been cut out of the monetization chain entirely, receiving as little as 8% of wagering revenue while third-party platforms pocket the rest and own the consumer data. That structural inequity is large, well-documented, and now addressable through a proven commercial deployment.

At a sub-$20M market cap, even a modest build-out to 15–25 facility relationships would represent a 4–8x return on conservative assumptions. The stock remains highly speculative, OTC-listed, early-stage commercial, and thin-float, and should be sized accordingly. But the risk/reward equation has improved materially since our initial thesis.

The pivot to watch: deal two and deal three. The Aambé agreement proves the model. Replication proves the platform.

DISCLOSURE: Long $BGTTF. This document is for informational purposes only and does not constitute financial advice. All investments involve risk, including the possible loss of principal. The author holds a position in the securities discussed.

This article reflects personal research and opinions and is provided for informational purposes only. It is not financial advice, a recommendation to buy or sell any security, or a consideration of your individual circumstances. Investing in small-cap and pre-commercialization companies involves significant risk, including the risk of total loss. Always do your own research and consider speaking with a qualified financial professional before making investment decisions.

Stay Informed with The Wire

Get the latest insights and analysis on public companies delivered directly to your inbox.