Heavy Oil Upgrading: Technology Potential, Global Deposits, and Aduro’s Hydrochemolytic System

This article explores Aduro Clean Technologies’ Hydrochemolytic Bitumen Upgrading (HBU) technology and its potential to transform heavy oil economics. By lowering costs and emissions, it could unlock vast Western Hemisphere reserves and reduce reliance on Middle Eastern crude. While promising, the technology remains pre-commercial, requiring validation at scale.

The world possesses a vast, underutilized reservoir of heavy oil and bitumen with most of it in the Western Hemisphere, not the Middle East. The central challenge has always been economics and emissions: converting thick, low-value feedstock into marketable crude is costly, energy-intensive, and carbon-heavy using conventional methods.

A new low-temperature, water-based technology - Aduro Clean Technologies’ (Nasdaq: ADUR) (CSE: ACT) Hydrochemolytic Bitumen Upgrading (HBU) system - aims to change this equation. If proven at commercial scale, such technologies could unlock billions of stranded barrels, reduce North America’s energy costs, and meaningfully decrease geopolitical dependence on Middle Eastern oil.

Here is an extensive interview with Aduro Clean Technologies CEO Ofer Vicus, mainly covering the company's progress toward commercialization of its plastic recycling vertical. It's well worth a watch to get an idea of the company's timeline. The video should start at the section (20:19 mark) where he discusses the oil upgrading vertical and the concept of Hydrochemolytic™ technology as a wide-ranging platform rather than an application-specific approach.

https://youtu.be/JaVEW6ztCeg?si=Px0hyMF9NqmK4PaN

The Strategic Potential of Better Bitumen Upgrading

The 2026 global energy landscape underscores why upgrading technology matters. Ongoing conflict in the Middle East has taken more than 12 million barrels of oil equivalent per day offline, including approximately 7 million barrels per day (bpd) of crude—roughly 7% of global liquids demand. The Strait of Hormuz, through which 20% of global oil and gas exports normally pass, has faced severe disruption. War-related damage to LNG trains, refineries, and fuel terminals across the Persian Gulf could exceed $25 billion, with recovery timelines measured in years.

This context highlights a fundamental vulnerability: decades of reliance on Middle Eastern light crude created exposure that cannot be remedied quickly. Yet the world’s largest unconventional oil reserves are in Canada and Venezuela, geopolitically more stable and capable of supplying enormous volumes if production and upgrading economics improve. A transformative upgrading technology would be not just an energy efficiency win, but a geopolitical rebalancing.

The scale is remarkable. Canada holds approximately 169.7 billion barrels of proven reserves, with 96% in oil sands. Alberta’s Athabasca oil sands alone contain Earth’s largest known bitumen deposit, with the McMurray reservoir estimated at 70.4 billion barrels originally in place. Total bitumen production in 2024 reached 3,558 thousand bbl/d, forecast to reach 3,639 thousand bbl/d by 2034. Venezuela’s Orinoco Belt contains an estimated 513 billion barrels of recoverable heavy oil, representing 90% of global extra-heavy oil on an in-place basis.

These deposits comprise the world’s largest heavy oil resource base, but much remains stranded due to economic and emissions challenges. Conventional upgrading is so expensive that full-scale synthetic crude facilities require billions in capital, making many projects marginal at current oil prices.

How Heavy Oil Differs from Conventional Crude

Heavy oils are classified by API gravity: conventional heavy oil falls in the 10°–22° API range, while extra-heavy oils and bitumen have API gravity below 10°. Bitumen from Athabasca typically has 6°–10° API gravity, viscosity averaging 100,000 centipoise (cP), and is effectively immobile at reservoir temperatures.

This creates two fundamental problems:

- Pipeline transport: Raw bitumen cannot flow without dilution with expensive lighter hydrocarbons (diluent) or upgrading to lighter product.

- Refinery processing: Most conventional refineries are configured for lighter crude; heavy, high-sulfur bitumen requires specialized processing.

The economic cost is substantial. Diluent must be added at ~0.44 barrels per barrel of bitumen, adding more than $10/bbl in operating costs. Diluent often trades at a premium to WTI, and transporting the blend consumes valuable pipeline capacity. Partially upgraded bitumen can fetch $10–15/bbl premium over diluted bitumen (dilbit).

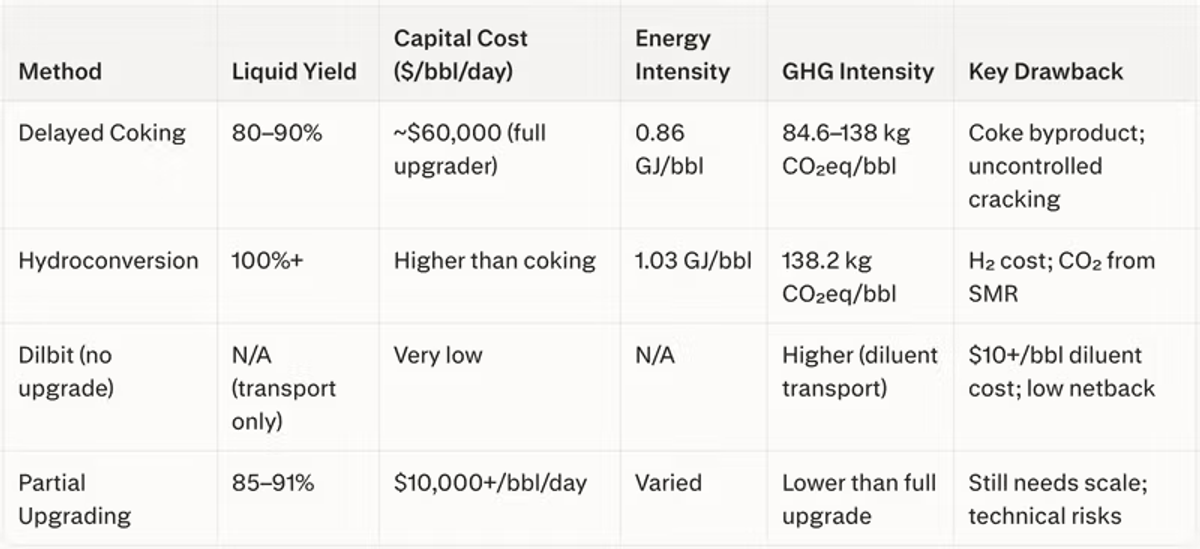

Current Methods of Upgrading Heavy Oil and Bitumen

Conventional upgrading falls into two categories: carbon rejection and hydrogen addition. Both face significant cost and emissions drawbacks.

Delayed coking is the most widely deployed in Canada’s oil sands. Bitumen is thermally cracked at 475–520°C, driving off lighter fractions and depositing carbon as petroleum coke—a low-value byproduct. Fluid coking and Flexicoking are continuous variants improving thermal efficiency, but fundamental limitations remain.

Hydroconversion adds hydrogen under high pressure and elevated temperature, converting molecules to lighter fractions without significant coke formation.

Diluent blending is the non-upgrading option. Approximately 60% of Alberta’s oil sands production historically ships as diluted bitumen (dilbit), which is raw bitumen blended with condensate or synthetic crude.

- Cost penalty: >$10/bbl operating cost; diluent often priced at WTI premium

- Pipeline inefficiency: ~30% of dilbit volume is condensate—wasted capacity

- No value enhancement: Dilbit carries discount versus SCO or partially upgraded bitumen

Summary of Current Methods

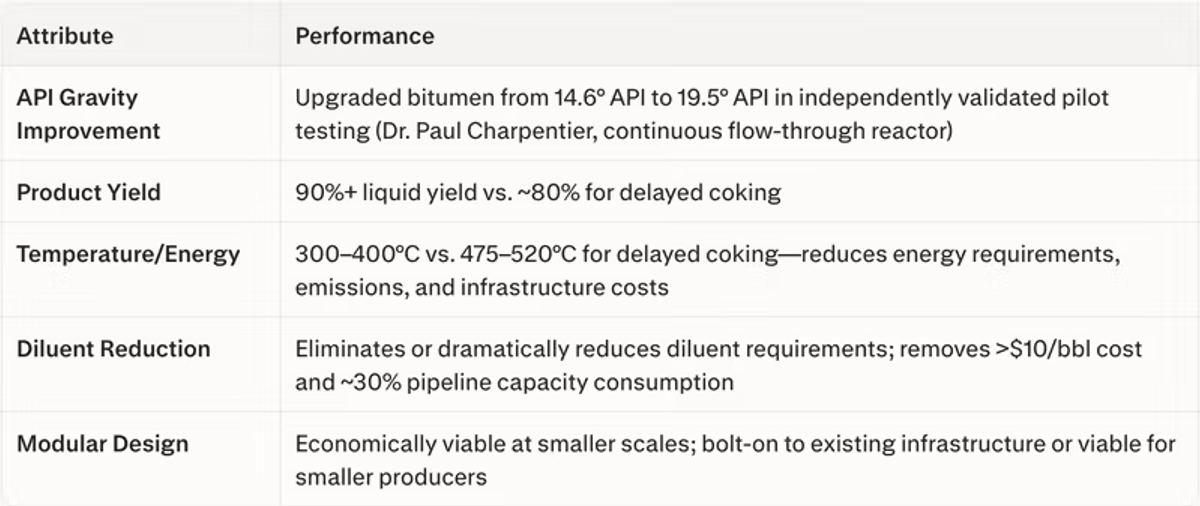

Aduro Clean Technologies’ Hydrochemolytic Bitumen Upgrading (HBU) System

Aduro Clean Technologies developed patented Hydrochemolytic™ Technology (HCT), applied to bitumen through its Hydrochemolytic Bitumen Upgrading (HBU) module. The core chemistry differs fundamentally from conventional methods.

Conventional thermal cracking applies heat as a “hammer” to break molecular bonds, producing uncontrolled fragmentation requiring separate stabilization using industrial hydrogen gas (H₂)—largely produced by steam methane reforming, a CO₂-emitting process. HCT uses simple, inexpensive metal compounds combined with small amounts of water and a low-cost organic co-reactant (the “H-source”), typically bio-based materials like ethanol, glycerol, or cellulose. These work like “scissors,” selectively cutting carbon-carbon bonds at much lower temperatures (300–400°C) while simultaneously stabilizing cleaved fragments before recombination .

A critical discovery: trace metals naturally present in bitumen (which are ordinarily nuisance contaminants) serve as effective catalysts and eliminate the need for expensive external catalysts. Using bio-based H-source instead of fossil-fuel-derived H₂ removes the CO₂ penalty from hydrogen production.

Key Technical Performance

Important Caveats: HBU remains in the pilot/pre-commercial stage. While independent validation confirmed proof-of-concept and major players (Shell, TotalEnergies, Prospera) are actively evaluating, commercial-scale cost-per-barrel data and fully benchmarked lifecycle emissions aren’t yet publicly available. Aduro’s 2024 revenue was $337,516 CAD; the company is still scaling up. Investors should distinguish between demonstrated lab/pilot performance and unproven commercial economics at scale.

Geopolitical Implications: Could Better Upgrading Reduce Middle East Dependence?

Technology dramatically reducing upgrading cost and emissions for Western Hemisphere heavy oil could meaningfully reduce global dependence on Middle Eastern light crude, but the mechanism is nuanced. Middle Eastern light crude and Canadian/Venezuelan heavy oil aren’t identical products. Most refinery infrastructure was built for light, sweet crude. Heavy oil from Canada/Venezuela typically trades at $10–20/bbl discount versus WTI because fewer refineries can efficiently process it. However, upgrading technology converting heavy bitumen into fungible medium crude at competitive cost would expand global supply of refinery-ready oil from non-OPEC, non-Middle Eastern sources.

Canada produces ~3,558 thousand bbl/day of bitumen and holds 81% of the world's recoverable bitumen. Athabasca alone can sustain current production for 185 years. If economically viable upgrading enables more bitumen to reach global markets as competitive crude rather than being stranded, it would add substantial non-OPEC supply.

The Atlantic Council frames the Western Hemisphere as an emerging “energy powerhouse” with potential to reshape global supply balances. U.S. shale + Canadian oil sands with improved upgrading + potentially revived Venezuelan production represents Western Hemisphere supply base dwarfing anything previously considered viable. But there is much ground to be covered and money to be invested before that vision can become a reality.

Conclusion

Improved heavy oil and bitumen upgrading technology holds significant economic and geopolitical potential. The world’s largest oil deposits outside the Middle East are in the Western Hemisphere, consisting predominantly of heavy oil and bitumen. Current upgrading methods (delayed coking, hydroconversion) are expensive, capital-intensive, emissions-heavy, and require large economies of scale pricing smaller operators out.

Aduro’s HBU system represents a genuinely novel approach: lower operating temperatures, bio-based hydrogen replacement, modular design, and higher product yields vs. legacy methods. The technology remains pre-commercial; investors should weigh pilot-stage performance against commercial scale-up challenges.

If HBU or similar technologies achieve commercial viability, they could meaningfully reduce the >$10/bbl diluent cost burden on Canadian producers, unlock stranded reserves, lower greenhouse gas intensity vs. conventional upgrading, and contribute to Western Hemisphere energy resilience. The geopolitical dividend of reducing global dependence on Middle Eastern crude would be incremental rather than immediate, but strategically significant over a decade-long horizon.

Author’s Disclosure: This article reflects the author’s independent analysis and personal views. It is not affiliated with or endorsed by Aduro Clean Technologies or any related party. The content is provided for informational purposes only and should not be considered financial or investment advice. Readers are encouraged to conduct their own independent research and due diligence before making any investment decisions.

This article reflects personal research and opinions and is provided for informational purposes only. It is not financial advice, a recommendation to buy or sell any security, or a consideration of your individual circumstances. Investing in small-cap and pre-commercialization companies involves significant risk, including the risk of total loss. Always do your own research and consider speaking with a qualified financial professional before making investment decisions.

Stay Informed with The Wire

Get the latest insights and analysis on public companies delivered directly to your inbox.