The Investors Who Made the Most Money Never Sold

This article highlights Aduro Clean Technologies as a compelling long-term opportunity supported by multiple independent analyses, including DCF, EV/EBITDA, technical trends, and rising institutional interest. A recent MOU marks a strategic shift toward a scalable, licensing-driven model. While significant upside may come through milestone-driven re-rating, investors must be prepared for volatility and execution risk.

Disclosure: I am a long shareholder in Aduro Clean Technologies (Nasdaq: ADUR | CSE: ACT | FSE: 9D5). This article incorporates independent third-party analysis reviewed and verified against publicly available sources. All price targets and projections are speculative and forward-looking. Not financial advice. Do your own due diligence.

This piece pulls together a DCF model, an EV/EBITDA framework, an institutional ownership chart, a technical setup, and a milestone re-rating roadmap, all produced independently by different people, all pointing in the same direction. My goal is to be the through-line.

I won’t claim to be the only person doing interesting work on Aduro Clean Technologies. Over the past few weeks, I have come across a DCF model, an EV/EBITDA valuation tool, institutional ownership data, and a re-rating catalyst framework, all produced independently, all pointing in the same direction.

My purpose in this article is not to originate all the thinking. It is to be the through-line. To pull the best independent work together, connect the dots, and give you a single place to see why so many people who have done the math are arriving at similar conclusions.

This is what conviction built on research actually looks like. Not one person’s model. A convergence.

First, the Psychological Framework

There is a story about Walmart that I keep coming back to.

Walmart’s stock increased from less than one cent to over $140. The return is almost incomprehensible — one of the greatest wealth-creation events in the history of the stock market.

Who actually captured that return?

The Walton family. Almost no one else. Because almost everyone else sold along the way. Nicholas Sleep, the legendary fund manager at Nomad Investment Partnership, wrote about this specifically: many companies ten-bag at some point in their lifetime, but even when you bought in early, the odds are you already sold when you tripled your money.

This is not a personal failing. It is a structural one. The human brain is wired to protect gains. When something you own doubles, the fear of losing that gain is more powerful than the logic of holding for ten times more. And at every single inflection point, every drawdown, every period of nothing happening, every moment where the market seemed to be telling you it was time to leave, the psychologically easy thing was to sell.

The Walton family could not sell. It was their company. That constraint, which looked like a limitation, turned out to be their greatest investment advantage.

The investors who made the most money in the greatest stocks of the last 40 years were, functionally, the ones who could not or would not look at the price.

What the Data Actually Shows

This is not just a Walmart story. Morgan Stanley’s Counterpoint Global research team studied 6,500 stocks listed on the NYSE and Nasdaq over the 40 years from 1985 to 2024, focusing on the 20 best-performing stocks over the entire period.

On average, those top 20 stocks delivered an annualized return of 19.3%, beating the S&P 500’s 11.8%. However, nearly all of them suffered losses of 55% or more from peak to trough at some point.

The median maximum drawdown was 72%. The median duration was 2.9 years.

Seventy-two percent. Nearly three years. For the best stocks on earth.

Apple dropped 83% during its roughest patch. Amazon fell 94%, from $5.4 million on a $100,000 investment down to $304,000, and took over 8 years to recover. These were not failing companies in their drawdown periods. They were the best companies in the world. The drawdown was not the signal to sell. It was the price of admission.

About 54% of stocks never return to par after hitting bottom. So the risk is real. The ones that recover are exceptional. And the only way to hold an exceptional one through its full arc is to hold it when it feels most like you should not.

This is the framework I apply before I go anywhere near a specific stock. The question is not whether a company looks interesting today. The question is: do I understand this business well enough to hold it through a 70% drawdown? If the answer is no, I should not own it at all.

Old Highs, New Support

I want to say something specific to anyone who bought Aduro near the $17 range and has felt the pullback.

There is a concept in technical analysis that long-term investors often overlook because they are focused on fundamentals. But it describes something real about how price psychology works.

Old highs become resistance. And then, once broken convincingly, they become support.

Every significant stock that has gone on to be a multi-bagger has gone through this cycle repeatedly. The price runs to a new high. It pulls back. The people who bought at the top feel pain. Some of them sell. The price consolidates. And then, if the underlying business is progressing, the old high gets tested again, broken, and the level that once felt like a ceiling becomes the floor for the next leg.

The $17 range is not a failure. It is a data point in a pattern that plays out in every stock that eventually goes much higher.

@TheProfInvestor, a technical analyst with over 85,000 followers at time of writing, posted a chart of $ADUR on March 17th with a simple caption: “One stock which gives me the ‘I will double’ vibe. I am serious.” The chart showed exactly this pattern: consolidation after the run-up, a wedge forming, and a measured move target flagged above the prior high. 30,000 impressions. The technicals and the fundamentals are telling the same story from different directions.

What matters is whether the underlying business is executing. And that brings us to what changed in March

Thanks for reading Penny Queen’s Newsletter! Subscribe for free to receive new posts and support my work.

Subscribe

What Actually Changed on March 19th

Aduro Clean Technologies announced an MOU with a leading global Engineering, Procurement, and Construction company to develop a commercial licensing package for Hydrochemolytic™ Technology.

Before March 19th: Aduro was a company with a validated technology, a running pilot plant, and a confirmed site for its first-of-a-kind industrial plant at Chemelot Industrial Park in the Netherlands.

After March 19th: Aduro is doing all of that — and simultaneously building the infrastructure to replicate that technology globally without funding every plant off its own balance sheet.

The MOU’s stated objective is a jointly developed commercial HCT license package and an associated license-driven business program covering how HCT solutions are marketed, priced, delivered, and supported for customers worldwide.

This is the Rolls-Royce model. Not the car, the jet engine division. Rolls-Royce does not own a single commercial aircraft. Airlines license the use of engines, paying per hour of flight, a model called Power by the Hour. The value is not in the metal. The value is in the knowledge of how to make the engine work. And that knowledge scales without limit.

That is what Aduro is building. Not “we will build every plant.” But “we will own the knowledge of how to make every plant run”… and the world pays to access it.

You cannot license something you cannot prove. Buried inside CEO Ofer Vicus’s quote in the press release were two lines that deserved their own headlines: the NGP pilot plant has recently transitioned to operating campaigns, and site selection for the FOAK industrial plant has been finalized.

The NGP is the instruction manual. The FOAK at Chemelot is the first full build from that manual. The MOU is the beginning of packaging both into something replicable everywhere. And the licensing model means replication does not require Aduro to raise capital for every new plant. Other operators bring their own capital. Aduro collects fees. The balance sheet does not scale with the ambition.

For shareholders, that matters enormously. The alternative, building every plant yourself, means dilution with every raise. It means shareholders waiting while the company manages construction risk in country after country. The licensing model compresses that timeline and protects the share structure.

The Independent Work

This is where I want to hand off to the people who have done serious quantitative work on this company, independently, without coordination, and without knowing each other’s conclusions in most cases.

The fact that they converge is not a coincidence. It is what happens when multiple people do the work honestly.

Piece 1: Why the Stock Is Priced Where It Is

Amateur Investing published a detailed DCF walkthrough using Aduro as a live example. His model is built around a key insight that most retail investors miss entirely: the reason the stock looks “cheap” at current prices is not that the market is blind. It is that the market is applying an extremely high discount rate, somewhere between 40–45%, because the technology is still transitioning out of the pre-revenue stage where that rate is standard.

As he explains it: at 40–45% discount rates, a company with Aduro’s long-term potential mathematically produces a share price in the $12–19 range. Which is exactly where the stock is.

The investment thesis is not “the market is wrong.” It is “the discount rate will compress as each milestone gets proven.” Here is how that ladder looks in his model:

• 45% discount rate (current — technology unproven at scale): ~$12–14

• 40% discount rate (technology de-risked, approaching first revenue): ~$14–19

• 30% discount rate (early revenues, business model emerging): ~$50–60

• 20% discount rate (scaling, established, private equity range): ~$200–300

• 10% discount rate (mature, low risk): ~$1,000

• 8% discount rate (fully de-risked): ~$1,000–2,000

Each milestone on the commercialization roadmap does not just move the stock because of the news. It moves the stock because it compresses the discount rate that rational investors apply to future cash flows. That is the re-rating mechanism.

Watch the full video here: Amateur Investing — Aduro DCF Model

Independent analysis. Not affiliated with Stock Therapy.

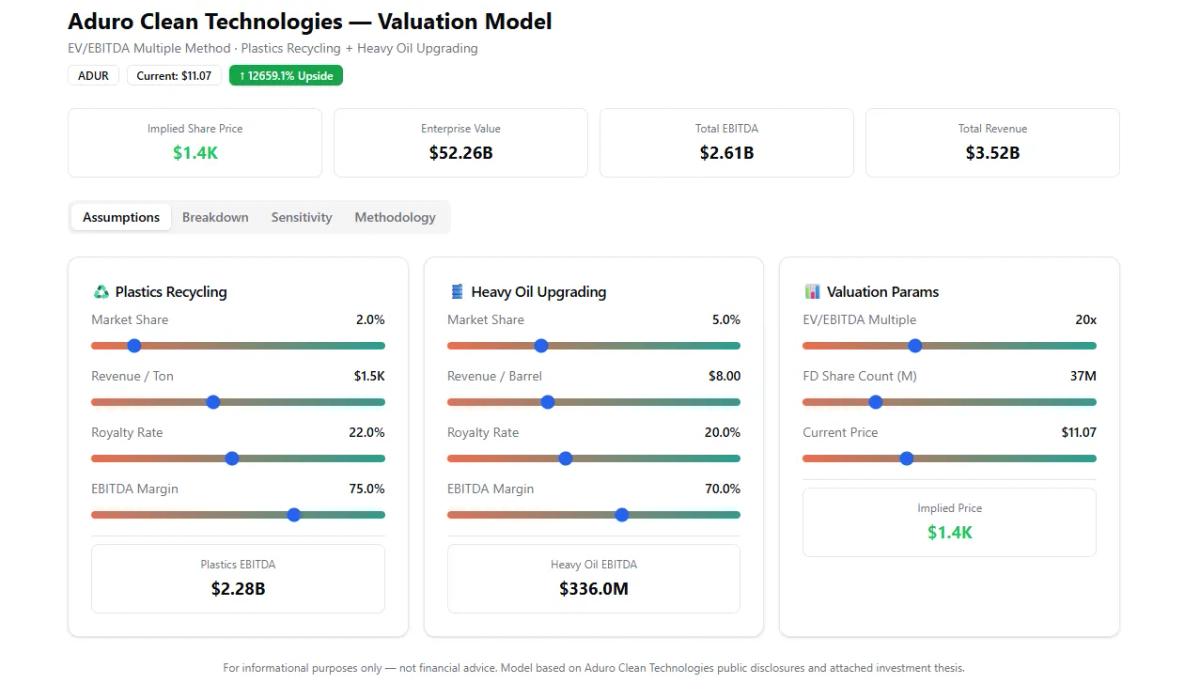

Piece 2: The EV/EBITDA Model — Including Heavy Oil Upgrading

A separate third-party valuation model by @perprins0 on X, built on EV/EBITDA methodology and covering both the Plastics Recycling and Heavy Oil Upgrading business lines, arrives at an implied share price of approximately $1,400 with a $52B enterprise value.

What makes this model worth noting is what it includes that most analyses ignore entirely: the Heavy Oil Upgrading vertical. Most models zero out HBU as “unmodelled optionality.” This one assigns it real value, 5% market share, $8/barrel royalty, 70% EBITDA margin, and still uses a conservative 2% plastics market share assumption on the recycling side.

Key assumptions:

• Plastics: 2% market share, $1,500/tonne revenue (top of management’s guided range), 22% royalty rate, 75% EBITDA margin → $2.28B EBITDA

• Heavy Oil: 5% market share, $8/barrel royalty, 70% EBITDA margin → $336M EBITDA

• Multiple: 20x EV/EBITDA, 37M fully diluted shares

• Implied price: ~$1,400/share

The model is interactive, you can adjust market share, royalty rates, and multiples and see what changes: Explore the interactive model here.

For informational purposes only. Not financial advice. Model based on Aduro public disclosures.

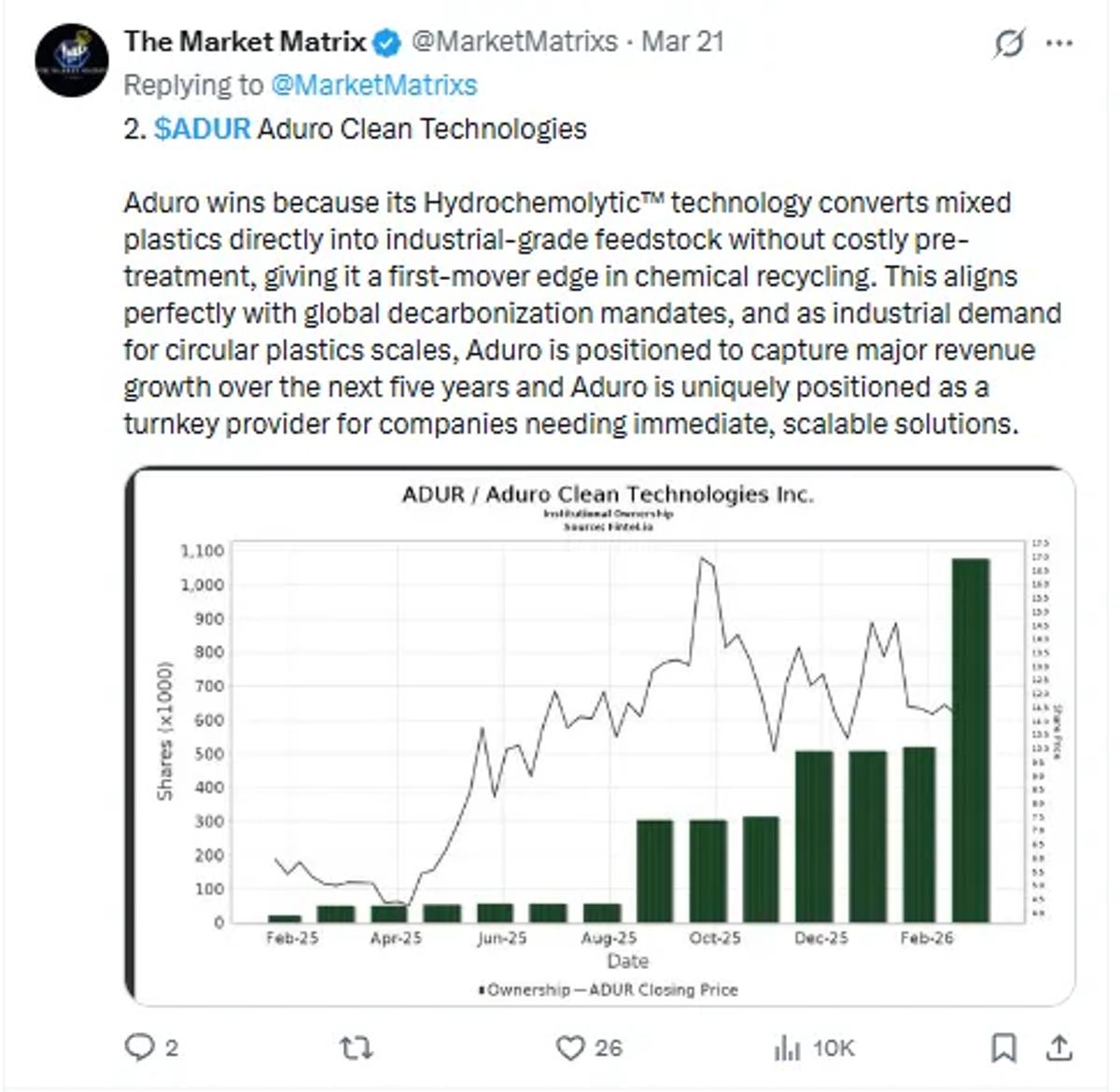

Piece 3: Institutional Ownership Building Quietly

The Market Matrix (@MarketMatrixs) recently flagged something worth paying attention to. The institutional ownership chart for ADUR shows a significant spike in accumulation through early 2026, right as the NGP hit operating campaigns and the FOAK site was confirmed.

Institutions do not accumulate quietly without doing diligence. That chart is not noise. It is a signal that the people who manage large pools of capital have done the work and are positioning ahead of the catalysts the rest of this article describes.

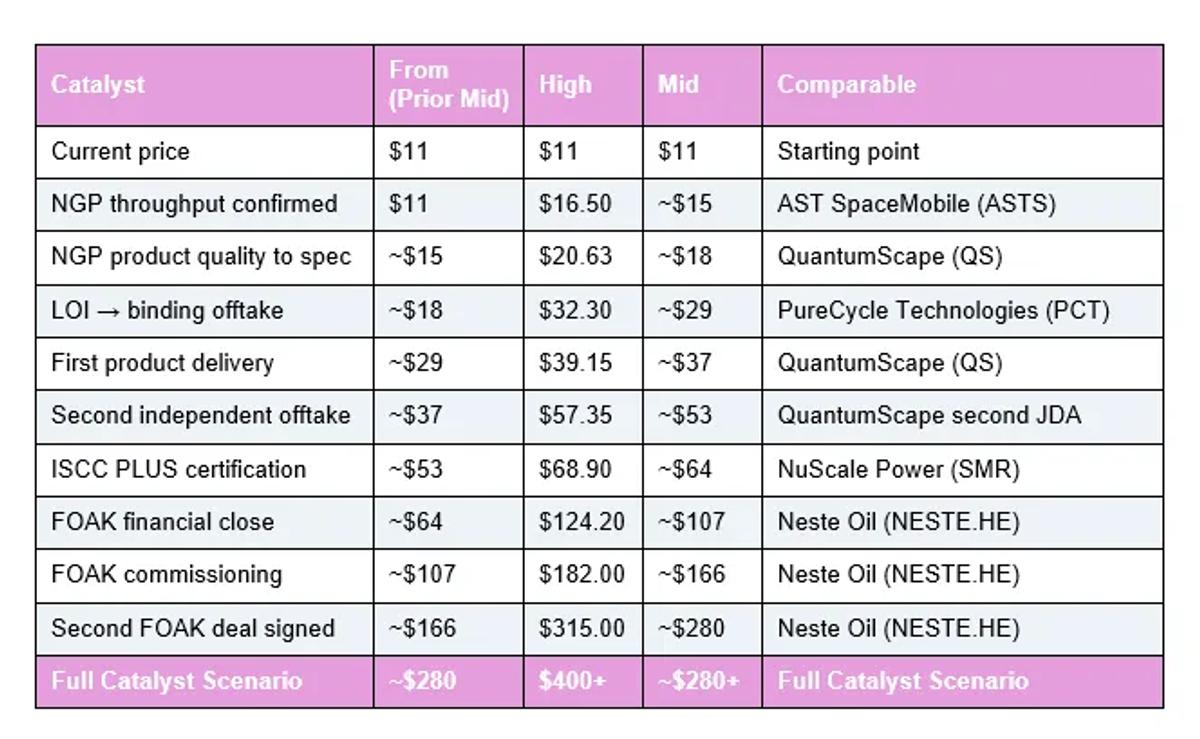

The Milestone Framework : How the Re-rating Could Unfold

This catalyst re-rating framework was forwarded to me by a member of my Discord community who wanted to remain anonymous. I fact-checked every real-world price movement it references against public data before including it here. The underlying comparable company evidence is sourced and verifiable.

The framework maps each commercialization milestone to a comparable company that experienced the equivalent event, and projects a price range based on documented market reactions. Each milestone removes a specific risk, compresses the discount rate, and unlocks a new pool of institutional buyers. (This is a speculative exercise, but useful for framing the potential.)

The table below uses each row’s starting point as the midpoint of the prior catalyst, a conservative, sequential framing rather than showing disconnected price ranges.

Full Catalyst Scenario

Tier 4 catalysts , analyst coverage initiation, institutional 13F disclosure, U.S. exchange uplisting: each add 20–60% to the prevailing price at the time of the event, additive to the above.

The comparables are not chosen for optimism. ASTS went from $2 to $39 when BlueWalker 3 proved direct-to-smartphone connectivity. QuantumScape surged roughly 200% in 2025 following the Cobra production milestone and first customer billings. NuScale reached a $57 all-time high following regulatory certification. Neste appreciated approximately 15x from its first plant commissioning in 2007 through 2019.

The critical difference between Aduro and Neste: Neste built and owned every plant. Aduro licenses the technology and collects royalties without owning the asset. In the replication phase, Aduro’s capital efficiency should be materially superior.

There are currently three sell-side analysts covering the stock: D. Boral Capital at $46, H.C. Wainwright at $22, and Ladenburg at $19. Consensus is approximately $29, meaning even the most conservative analyst sees the stock more than 70% higher from here. The milestone table above, the DCF model, and the EV/EBITDA framework all suggest the analyst consensus is itself conservative relative to what the business could become

The Part Most Investors Will Get Wrong

The Morgan Stanley data says the median drawdown for the best-performing stocks over 40 years was 72%. Not 20%. Seventy-two percent. Over nearly three years.

If you are holding something because you believe it could be 20x from here, you have to be psychologically prepared for it to first go to a price that feels like the thesis has failed. Because that is what happens, consistently, to the companies that ultimately win.

The Walton family held Walmart because they could not easily sell. Most investors do not have that structural constraint. They have to manufacture it themselves — through conviction built on understanding, not on price action.

I cannot tell you Aduro is one of the exceptions. The MOU is non-binding. The FOAK has not been built. The licensing model is a framework, not a revenue line. Real risk exists here, and anyone who tells you otherwise is not being straight with you.

What I can tell you is this: I have now seen a DCF model, an EV/EBITDA model, an institutional ownership chart, a technical analyst flagging a double setup, and a milestone-based re-rating framework, all built independently, all pointing in the same direction. That convergence is not something I manufactured. It is something I found.

Before March 19th, Aduro was working toward one plant. Today, they are working toward one plant and the blueprint to replicate it everywhere.

If that distinction matters as much as I think it does, the investors who benefit most will be the ones who held it like they forgot they had it.

Disclosure: I am a shareholder in Aduro Clean Technologies (Nasdaq: ADUR . I have held a position since the IPO. This article incorporates independent third-party analysis which I have reviewed and verified against publicly available sources. All price targets, model outputs, and milestone projections are speculative and forward-looking. Past performance of comparable companies does not guarantee similar results for Aduro. This article is for informational and educational purposes only and does not constitute financial advice. Always conduct your own due diligence before making any investment decision.

This article reflects personal research and opinions and is provided for informational purposes only. It is not financial advice, a recommendation to buy or sell any security, or a consideration of your individual circumstances. Investing in small-cap and pre-commercialization companies involves significant risk, including the risk of total loss. Always do your own research and consider speaking with a qualified financial professional before making investment decisions.

Stay Informed with The Wire

Get the latest insights and analysis on public companies delivered directly to your inbox.